Headlines

Industry News

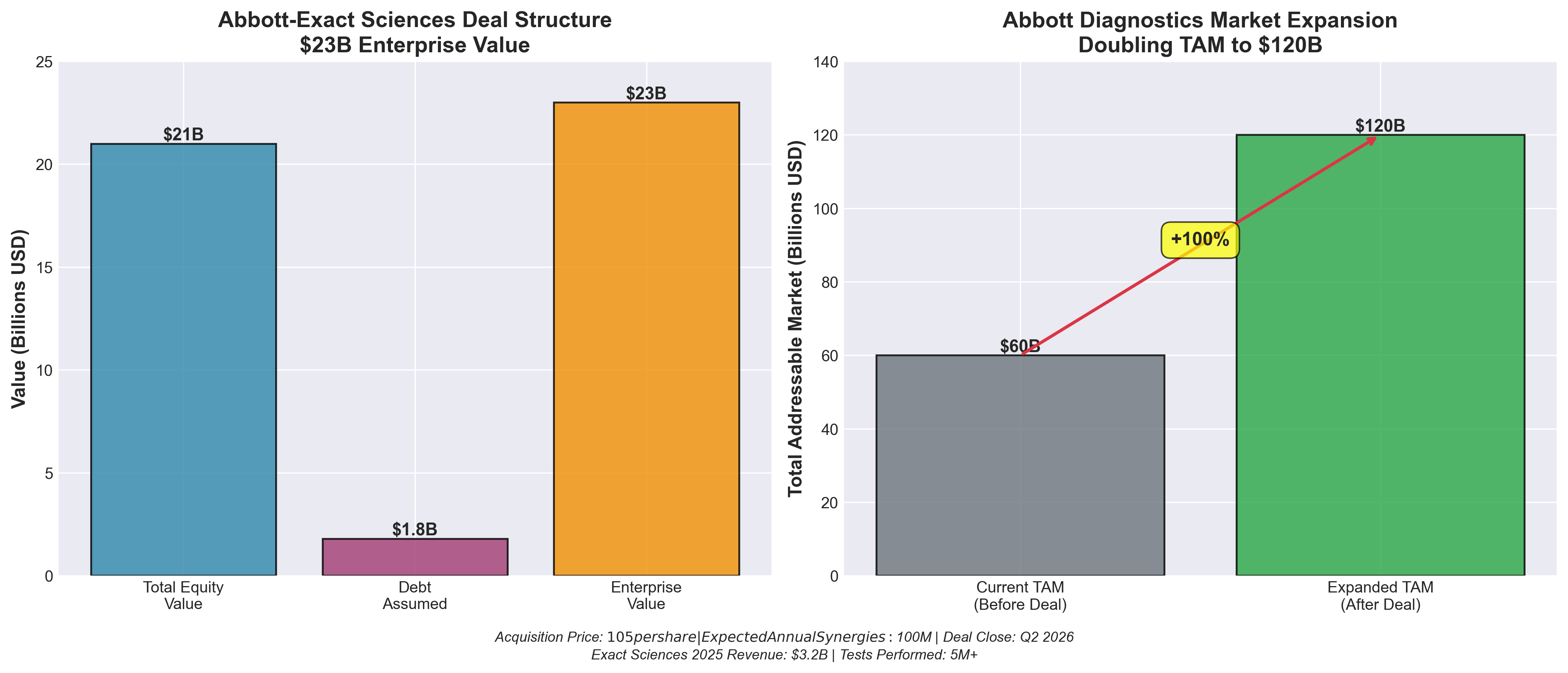

- Abbott dives into cancer diagnostics with $23B buyout of Exact Sciences

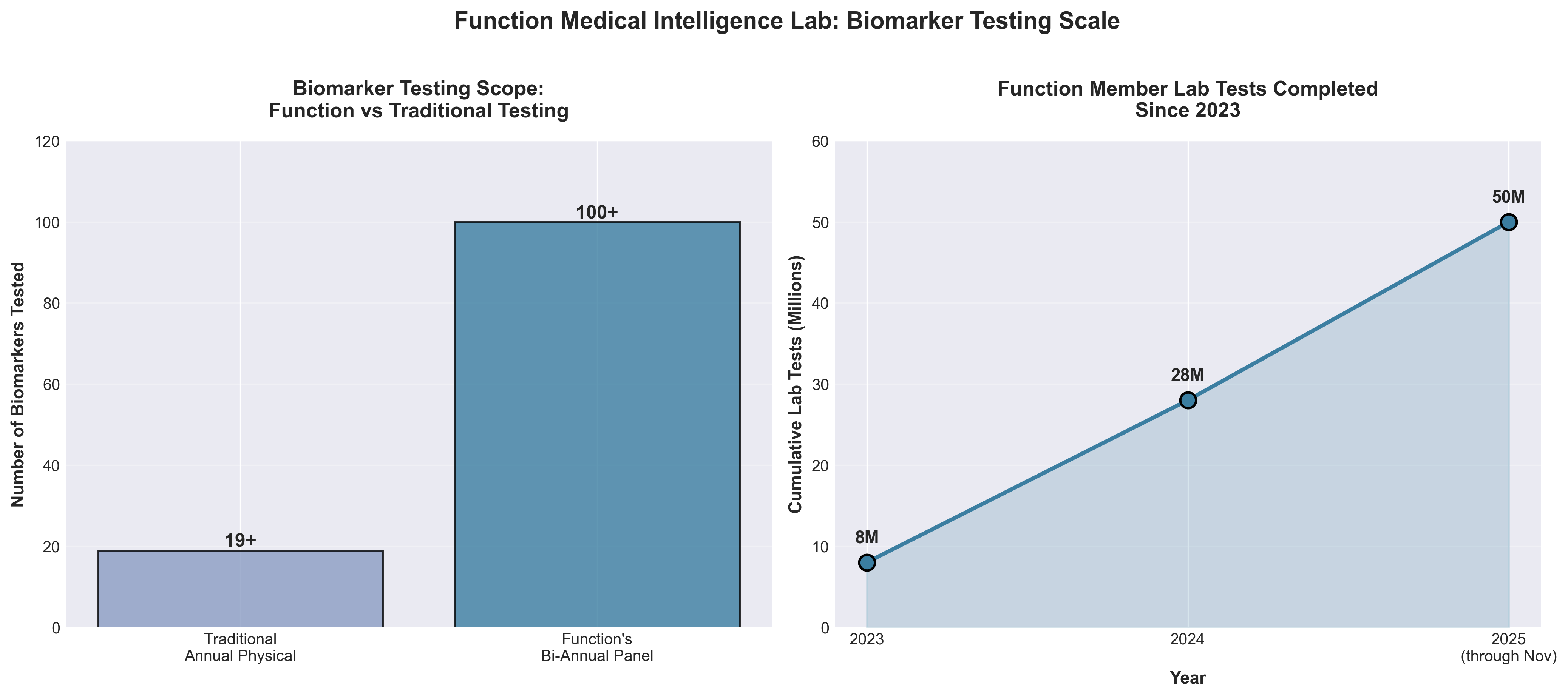

- Function Health raises $298M and launches Medical Intelligence Lab

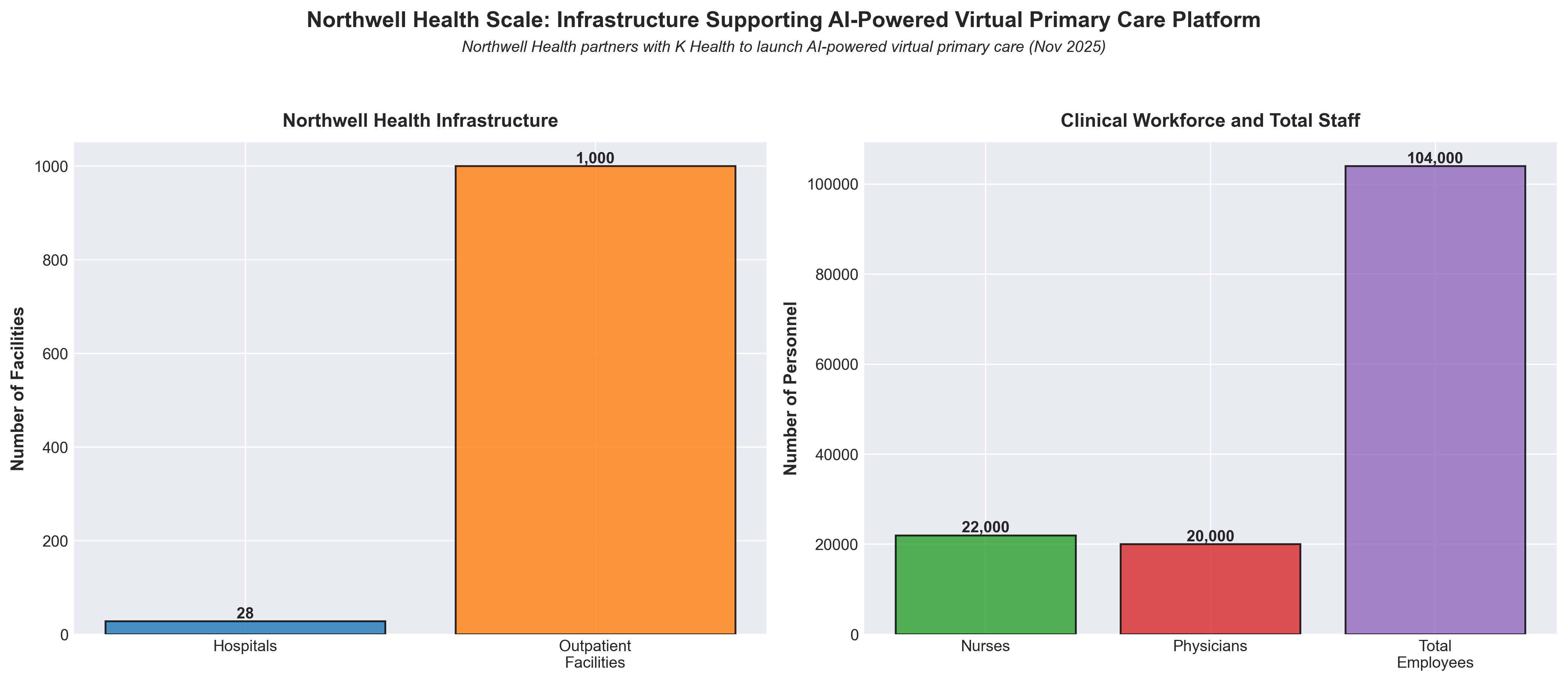

- Northwell Health and K Health Launch AI-Powered Virtual Primary Care Now Platform

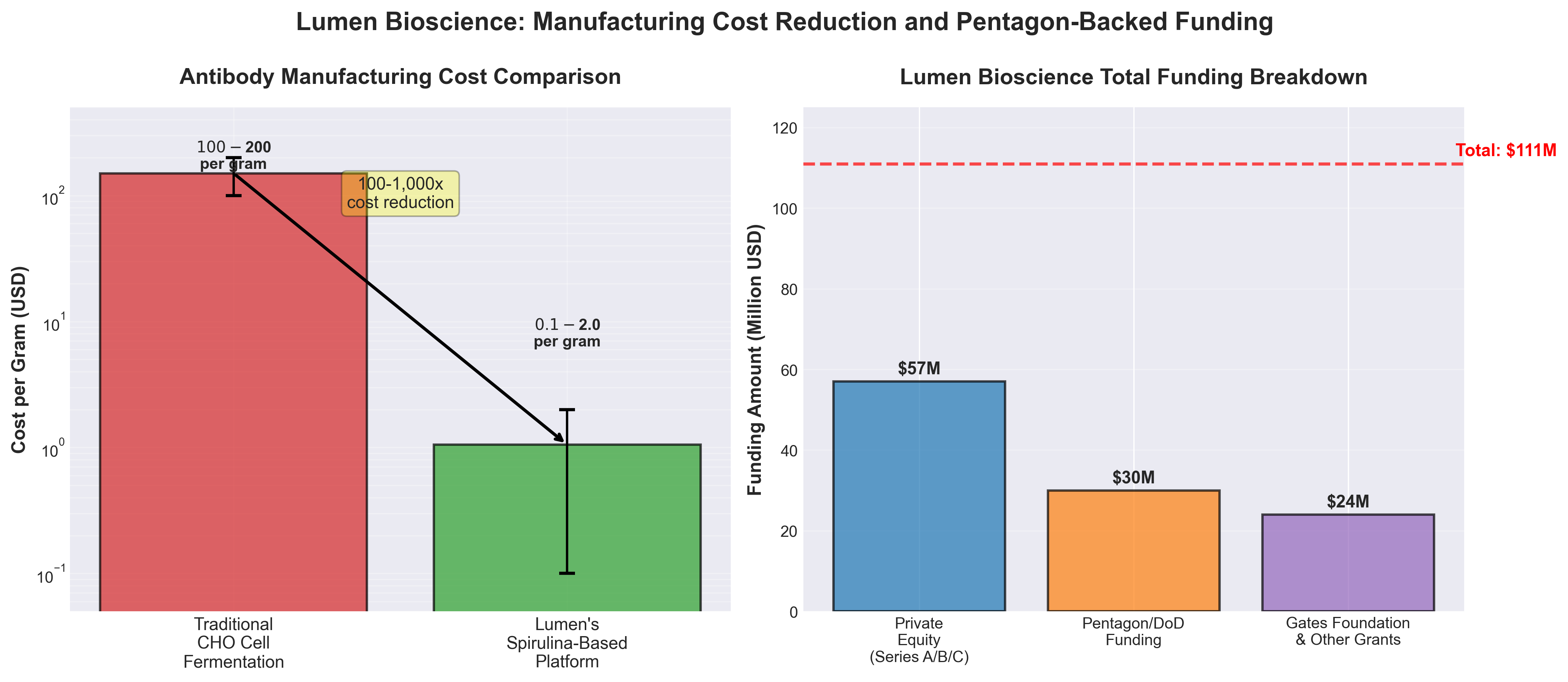

- Pentagon-backed Lumen Bioscience drastically slashing antibody manufacturing costs

Clinical Studies & Translational Reports

- Trends in AI-Enabled Clinical Decision Support Tools: Up-To-Date vs OpenEvidence

- Trends in Adoption of AI Across Healthcare

- Paradromics’ brain implant could rival Neuralink’s enters clinical trials

- Aspen Neuroscience gets $115M for Parkinson’s cell therapy

- Factor IX-Padua AAV gene therapy in hemophilia B: phases 1/2 and 3 trials

New Research

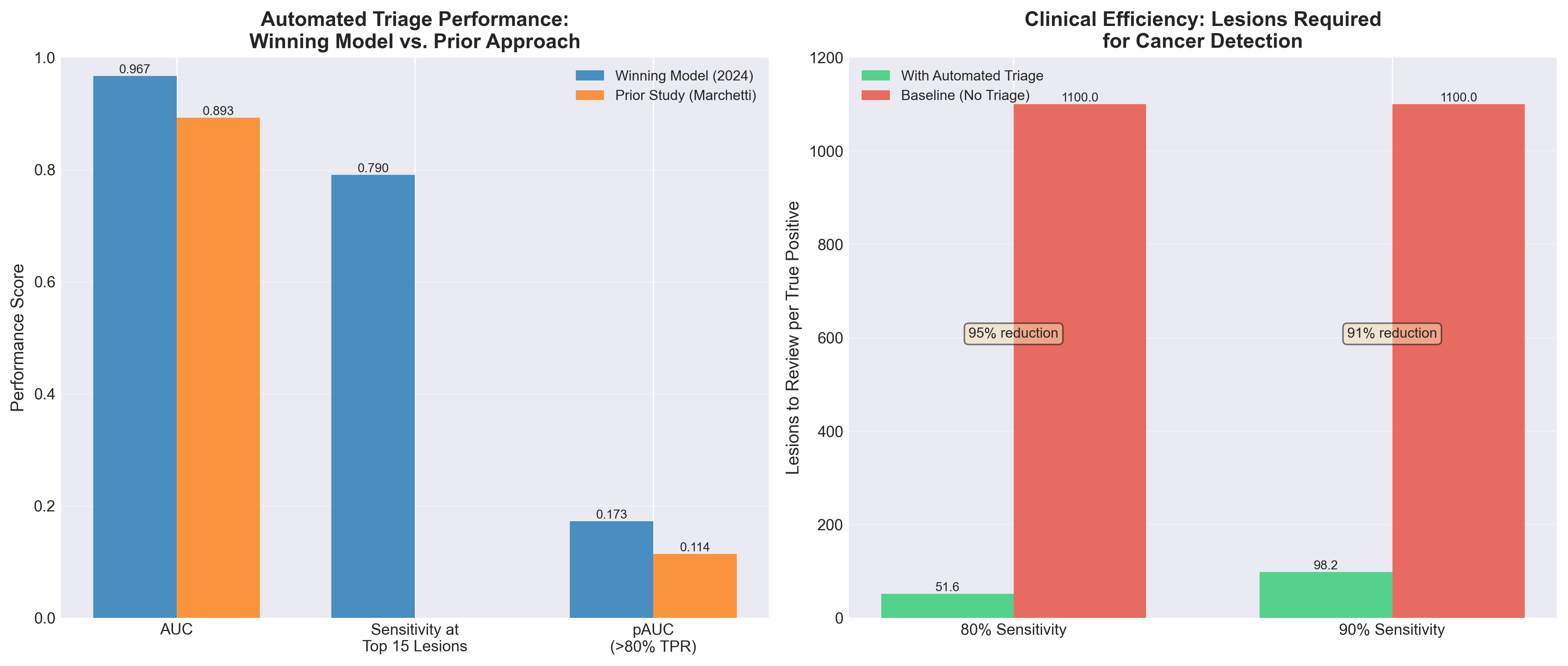

- Automated triage of cancer-suspicious skin lesions with 3D total-body photography

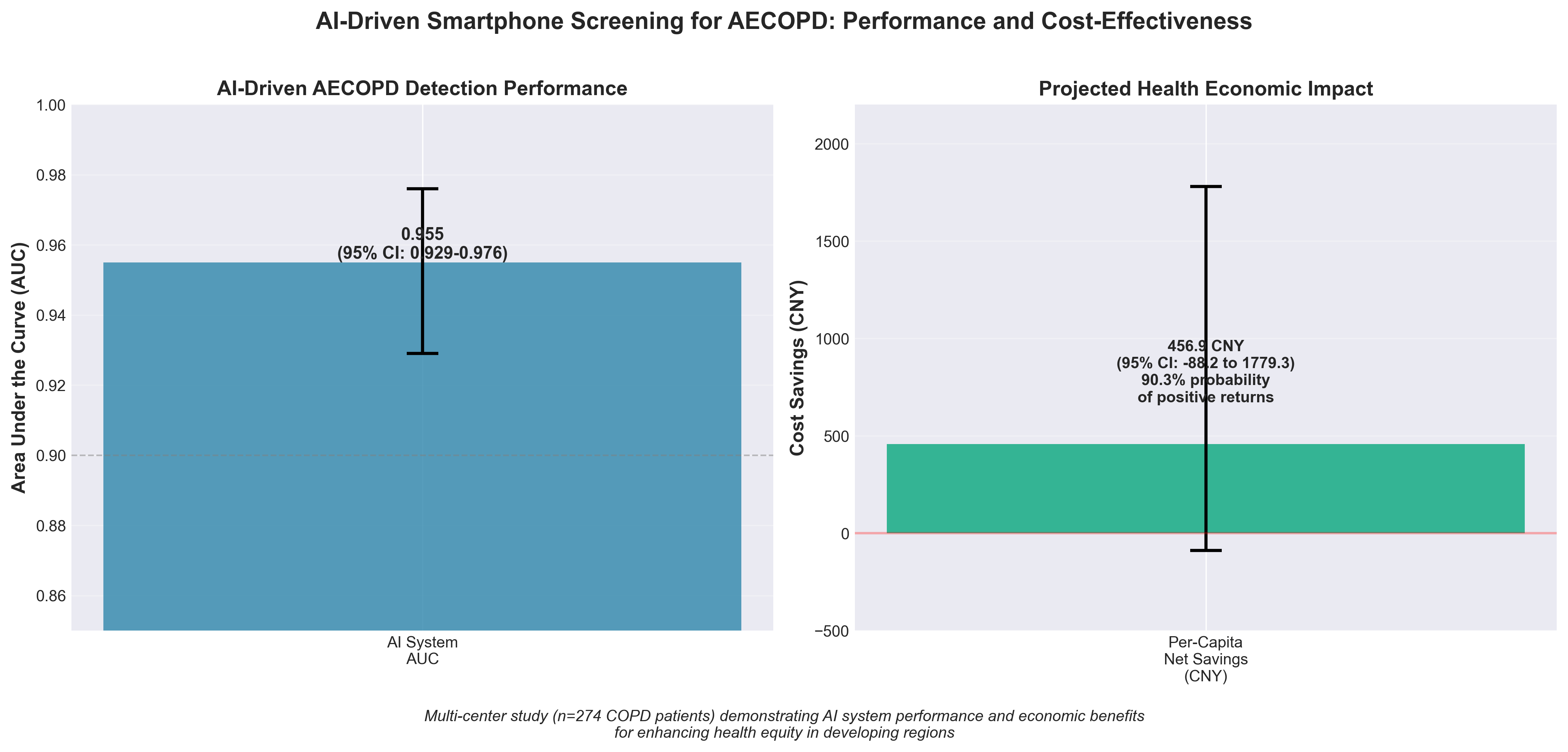

- AI-driven smartphone screening for acute COPD exacerbations

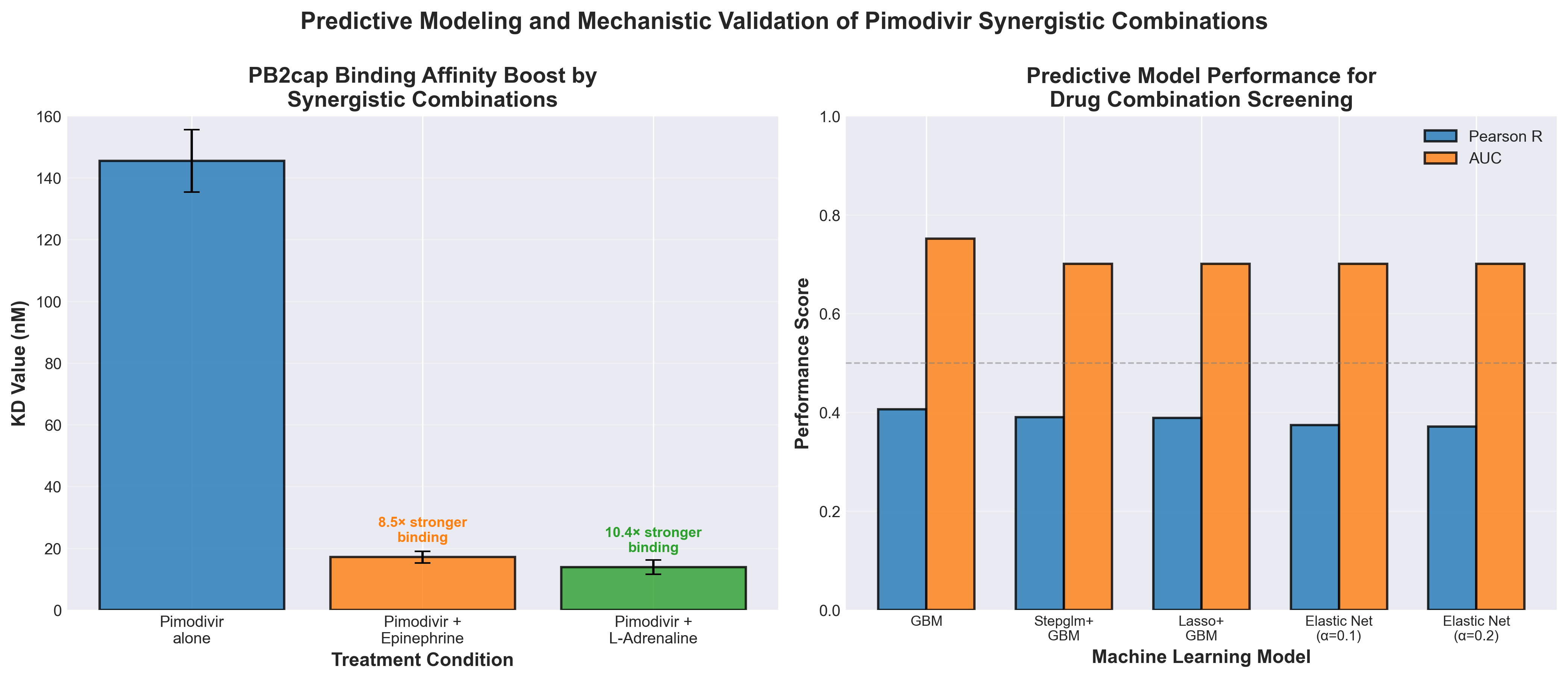

- Predictive modeling & validation of drug combinations for anti-influenza therapy

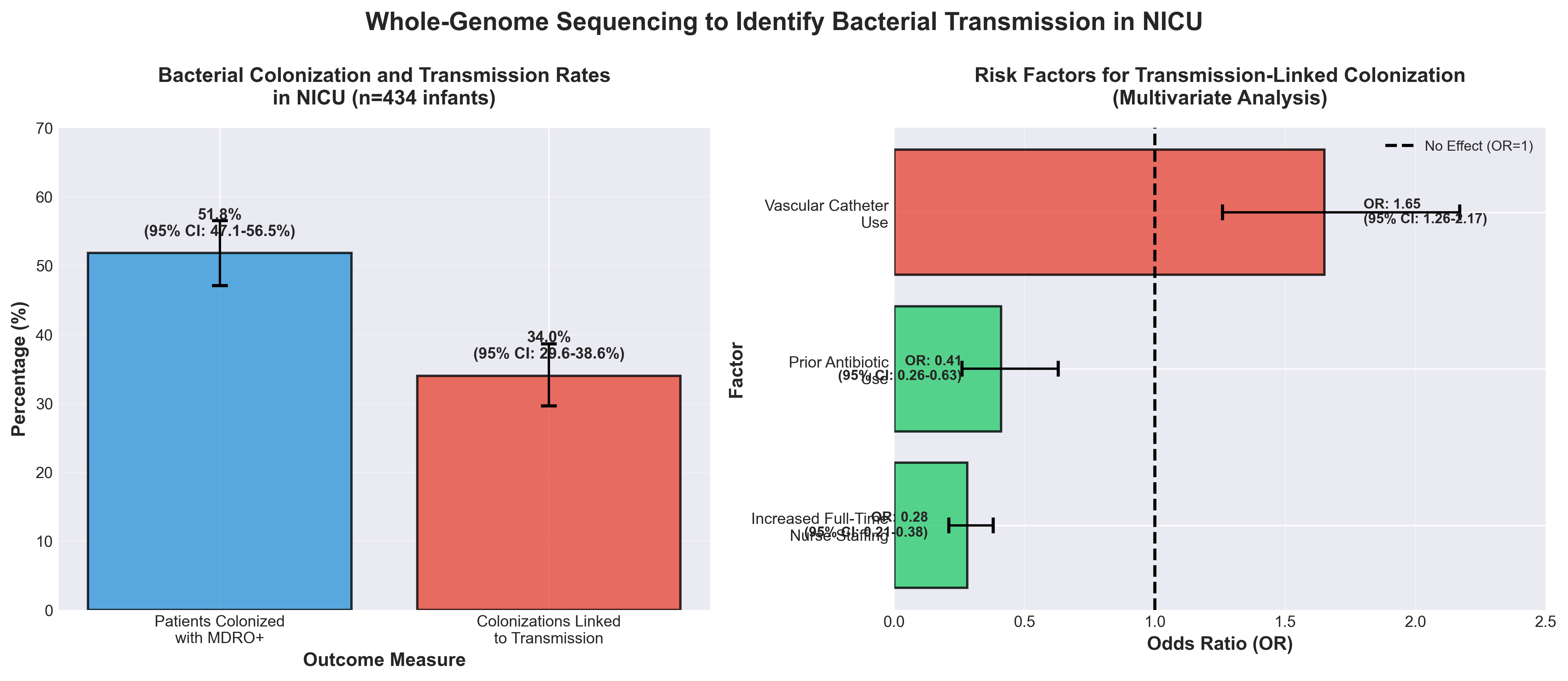

- Whole-Genome Sequencing to Identify Bacterial Transmission in Neonates

Industry News

1. Abbott dives into cancer diagnostics with $23B buyout of Exact Sciences

• Market Expansion Through Acquisition: Abbott is doubling its diagnostics TAM to $120B+ by acquiring Exact Sciences’ cancer screening portfolio, targeting 20M annual cancer diagnoses globally—this signals major pharma/diagnostics players will increasingly consolidate oncology diagnostic capabilities to capture the preventative/precision medicine segment.

• Revenue & Scale Validation: Exact Sciences’ $3.2B revenue run rate with 5M+ tests performed annually and accelerating growth across both existing (Cologuard) and new products (blood-based multi-cancer tests) demonstrates proven commercial traction that justifies the $23B valuation—companies should benchmark their cancer diagnostic pipelines against this scale to assess competitive positioning.

• Strategic Repositioning of Diagnostics Role: Abbott’s $100M annual synergy targets and emphasis on answering “three critical questions” (diagnosis, treatment selection, remission monitoring) reflects a shift toward integrated diagnostic solutions that span screening, prediction, and monitoring—this consolidation trend will likely pressure independent diagnostic companies to either specialize or seek acquisition.

2. Function Health Raises $298M and Launches Medical Intelligence Lab

• Scale validation of longitudinal biomarker monitoring: 50+ million lab tests completed since 2023 demonstrates market demand for preventive health panels beyond traditional care—actionable for competitors to prioritize multi-biomarker platforms and frequency-based testing models rather than single-point diagnostics.

• AI-driven integration of fragmented health data creates competitive moat: The Medical Intelligence Lab’s unified system combining 100+ biomarkers, imaging, wearables, medical records, and research creates a defensible advantage in early detection (cancer, cardiovascular disease, diabetes) that fragmented systems cannot replicate—companies should prioritize interoperability infrastructure and longitudinal data aggregation.

• Clinical credibility + AI adoption = market expansion: Leadership additions (Sodickson from NYU Langone, Lester in women’s health) alongside AI capabilities signals that clinical validation, not just technology, drives adoption—industry professionals should embed expert clinical guidance into AI outputs rather than deploying algorithms independently to gain trust in preventive health applications.

3. Northwell Health Partners with K Health to Launch AI-Powered Virtual Primary Care Now Platform

• Scale of Implementation & Market Validation: Northwell Health’s 104,000-person workforce across 28 hospitals and 1,000+ outpatient facilities adopting K Health’s AI demonstrates enterprise-wide integration potential; this partnership joins elite health systems (Mayo Clinic, Mass General Brigham, Cedars-Sinai), signaling clinical-grade AI viability for large-scale primary care delivery and establishing a proven operational blueprint for competitors.

• Workflow Efficiency Through Pre-Visit AI Triage: The platform’s AI Medical Chat completes patient intake before clinician encounters, reducing visit time and improving data quality—this physician-augmentation model (not replacement) directly addresses the primary care access crisis while maintaining clinical oversight, offering a replicable revenue and capacity optimization strategy for other health systems.

• System Integration as Competitive Moat: By embedding K Health’s AI within Northwell’s existing infrastructure and EHR ecosystem rather than operating as a standalone service, the partnership ensures continuity of care across virtual and in-person touchpoints; this integrated approach creates switching costs and demonstrates that fragmented point solutions face displacement risk in favor of systemically embedded platforms.

4. Pentagon-backed Lumen Bioscience is ready to drastically slash antibody manufacturing costs

• Cost reduction of 100-1,000x enables market expansion: Lumen Bioscience’s spirulina-based manufacturing reduces antibody production costs from $100-200/gram to potentially $0.10-2.00/gram, allowing treatment of 145x more patients per dollar spent—this fundamentally changes economic feasibility for large-scale therapeutic deployment and orphan disease applications previously considered unprofitable.

• $111M in funding (including $30M+ Pentagon backing) validates platform durability: DoD awards totaling $30M+ for LMN-201 clinical advancement and vaccine platforms, combined with $30M Series C led by Gates Foundation, signal institutional confidence in manufacturing scalability and dual-use biodefense applications that de-risks commercialization timelines.

• 15+ kg/week GMP capacity with clear clinical pathway reduces manufacturing risk: Fully integrated cGMP facility production capability positions Lumen to supply Phase 3 trials and potential commercialization without additional capital-intensive facility buildout, while focusing on C. difficile (5B+ annual market) addresses a high-prevalence, high-recurrence disease with 40-50% reinfection rates.

Clinical Studies & Translational Reports

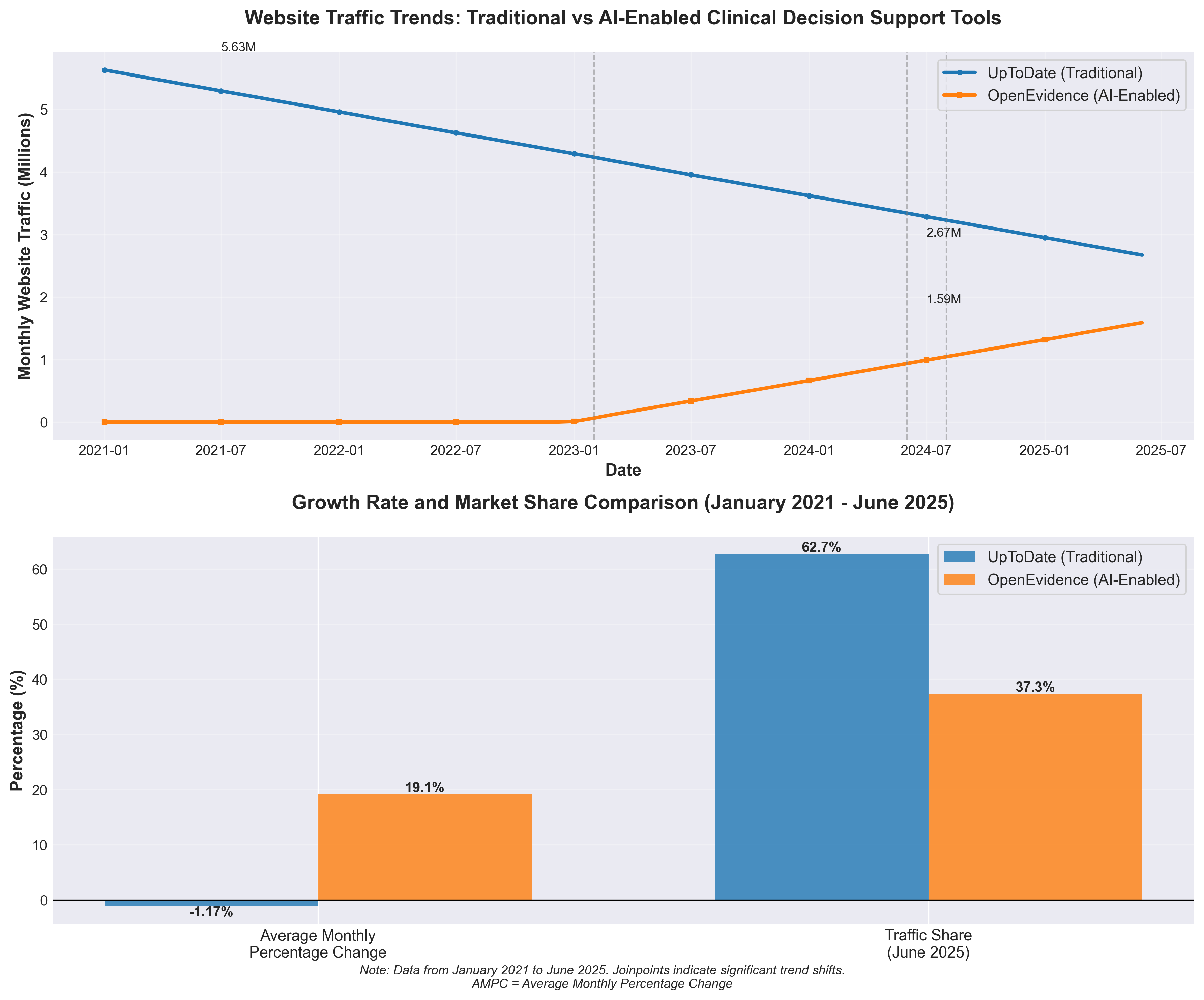

1. Public Interest in an AI-Enabled Clinical Decision Support Tool

• AI-enabled clinical tools are rapidly displacing traditional platforms: OpenEvidence search volume grew 5.13% annually while UpToDate declined 0.64% (P<.001), with OpenEvidence capturing 98.7% of AI clinical tool searches—signaling a significant market shift that companies should address through AI integration or risk obsolescence.

• Clinician adoption is accelerating with a clear inflection point: The joinpoint in June 2024 marks when AI clinical tool adoption accelerated substantially, suggesting the market has crossed a tipping point; organizations should prioritize validating and deploying AI-enabled decision support now rather than waiting for broader adoption signals.

• Canadian data validates competitive displacement, not just substitution: UpToDate searches remained stable in Canada (where OpenEvidence is unavailable) but declined in the US, confirming that AI tools are cannibalizing traditional platform usage rather than expanding the overall market—requiring vendors to decide between competing or partnering with AI platforms.

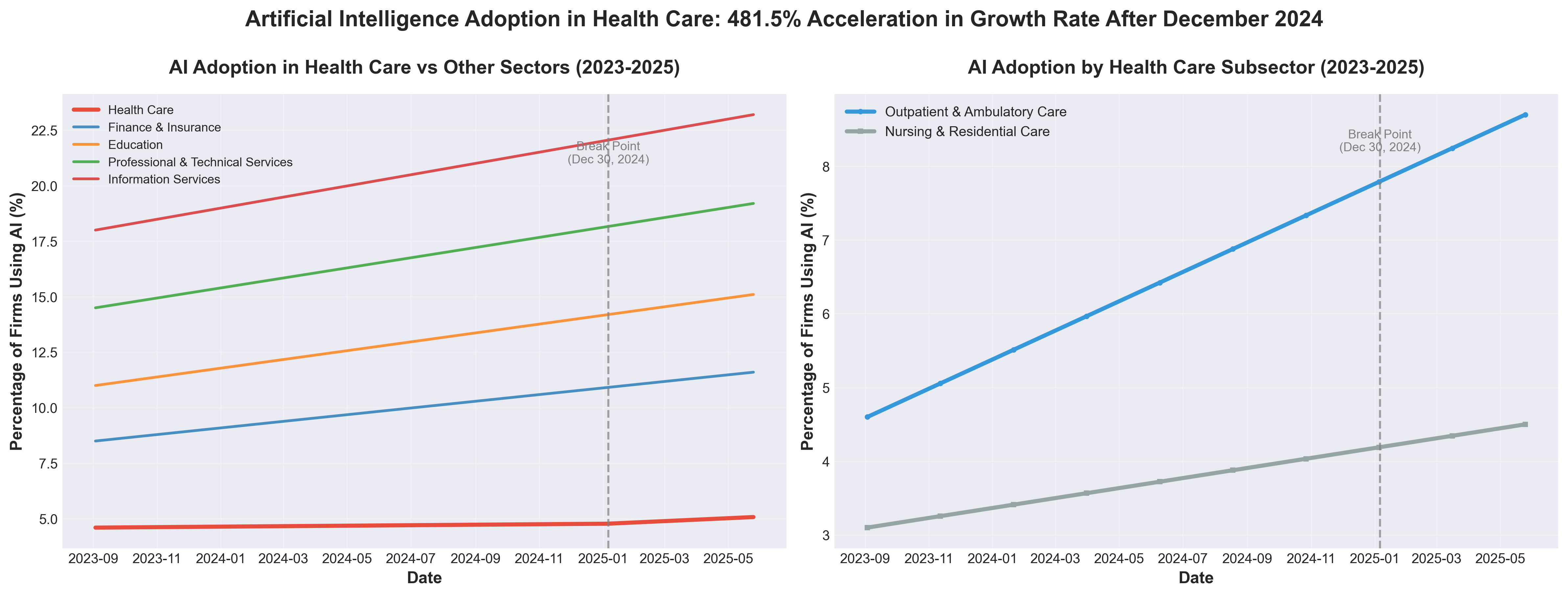

2. Adoption of Artificial Intelligence in the Health Care Sector

• Healthcare AI adoption significantly lags competitors: At 8.3% in 2025, healthcare firm AI adoption trails finance/insurance (11.6%), education (15.1%), and information services (23.2%)—indicating substantial competitive disadvantage and market opportunity for healthcare organizations to accelerate implementation.

• Accelerating adoption trajectory starting Q1 2025: AI adoption in healthcare shifted dramatically around December 2024-January 2025, with the rate of increase jumping 481.5% (from 0.005% to 0.03% biweekly growth), signaling this inflection point as critical timing for industry professionals to evaluate and deploy AI solutions before competitive saturation.

• Baseline adoption remains nascent across healthcare: With mean adoption at only 5.9% over the 21-month study period, the healthcare sector is still in early stages, presenting a window for organizations to establish differentiation through strategic early-mover AI investments in clinical documentation, patient engagement, and clinician support tools before adoption becomes standardized.

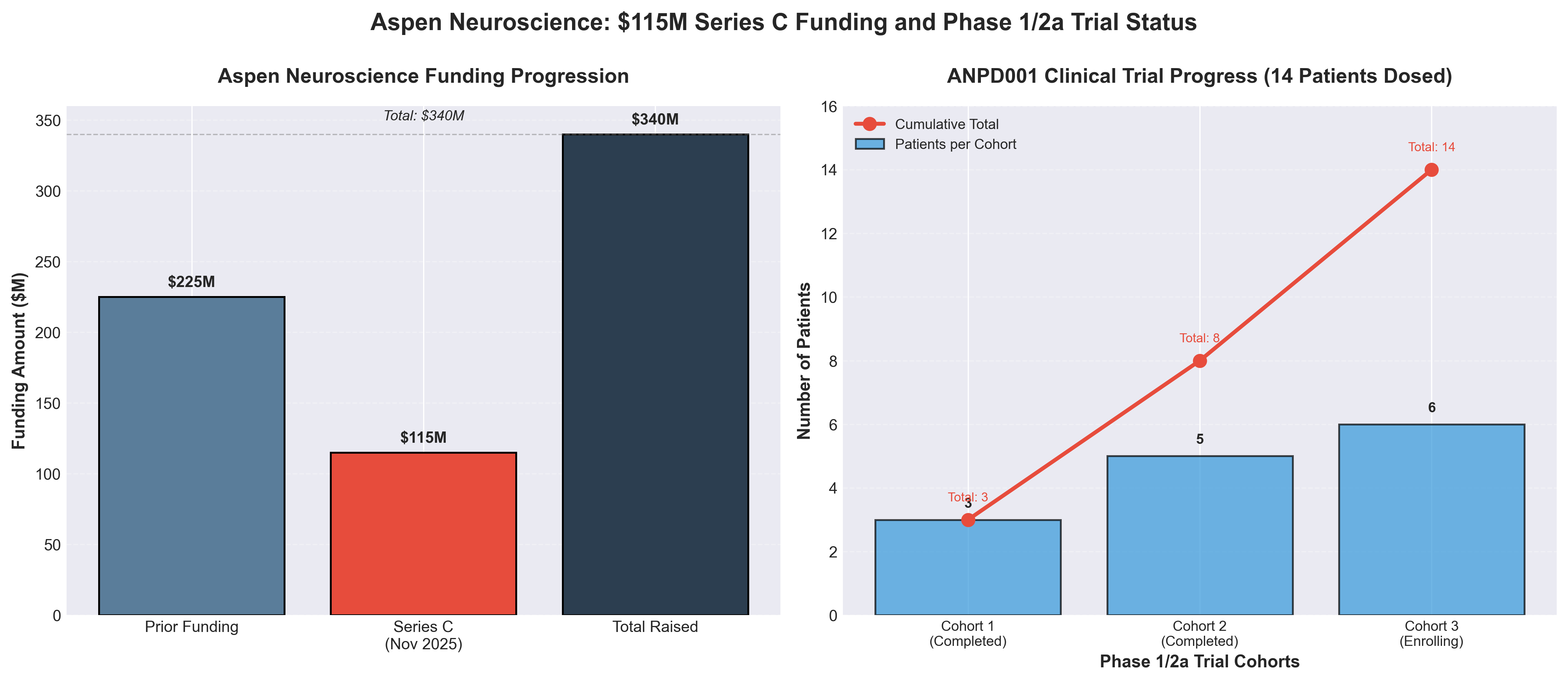

3. Aspen Neuroscience gets $115M for Parkinson’s cell therapy, potential IPO in sight next year

• Phase 3 Entry in 2026 with $340M Total Funding Positions Aspen for Near-Term IPO: With $115M Series C bringing total raised to $340M and FDA Phase 3 discussion planned for H1 2026, Aspen has sufficient runway to complete Phase 3 initiation and reach inflection points that typically trigger IPO windows (2027-2028), making this a high-probability exit candidate in a competitive cell therapy landscape where most programs are still in Phase 1/2.

• 14 Patients Dosed with Zero Serious Adverse Events Creates Strong Safety Profile for Regulatory Path: The completion of two dose-escalation cohorts with no serious adverse events reported, combined with positive 6-month efficacy data from the first 3 patients, significantly de-risks the Phase 3 pathway compared to competitor BlueRock (which already entered Phase 3 but faces 2028-2029 approval timeline), potentially enabling faster commercialization if efficacy signals hold.

• $46.26B Cell Therapy Market by 2034 (CAGR 21.46%) vs. $13.34B Parkinson’s Market Signals Adjacent Revenue Opportunities: The 7x market size differential between cell therapy broadly and Parkinson’s specifically suggests successful commercialization of ANPD

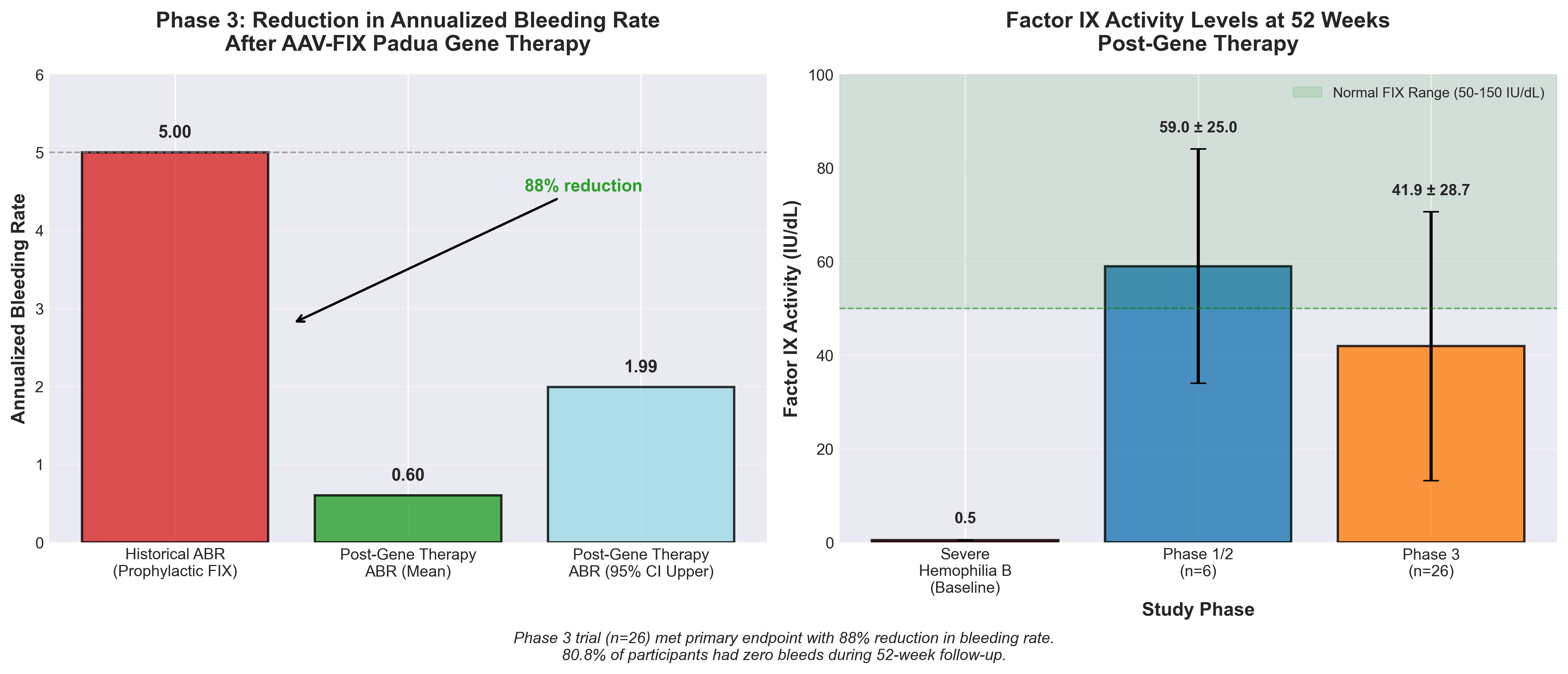

4. Factor IX-Padua AAV gene therapy in hemophilia B: phases 1/2 and 3 trials

• Durable efficacy with manageable safety profile establishes commercial viability: Phase 3 data showed 80.8% of patients achieved zero bleeds over 52 weeks with a mean ABR of 0.60, and the most common adverse event (transaminitis) occurred in only 33.3% of phase 1/2 participants with no grade 3 drug-related AEs, positioning BBM-H901 as a competitive one-time treatment alternative to lifelong prophylactic therapy.

• Chinese market validation addresses unmet need in on-demand therapy populations: This is the first large Phase 3 validation (26 patients) in China where most hemophilia B patients use on-demand rather than prophylactic treatment, representing significant market expansion potential beyond developed nations and addressing a geographically distinct patient population with different treatment paradigms.

• FIX-Padua’s sustained expression durability drives cost-benefit case: Achieving 41.9 IU/dL mean vector-derived FIX activity at week 52 with single-dose administration reduces treatment burden substantially compared to recurring factor replacement, which is critical for cost-effectiveness arguments in health systems evaluating gene therapy adoption.

New Research

1. Automated triage of cancer-suspicious skin lesions with 3D total-body photography

2. AI-driven smartphone screening for acute COPD exacerbations: enhancing health equity in developing regions

• Validated AI diagnostic tool with strong commercial potential: The smartphone-based AECOPD detection system achieved 0.955 AUC and demonstrated cost-effectiveness with 90.3% probability of positive ROI (projected per-capita savings of 456.9 CNY), creating a scalable, low-cost screening solution for markets with limited pulmonary specialist access.

• Addresses critical market gap in primary care: Only 19.4% of general practitioners in Shanghai could distinguish acute vs. stable COPD, indicating massive diagnostic failure at the point-of-care; this AI tool eliminates reliance on subjective patient reporting and provider expertise, directly solving a documented clinical bottleneck in developing regions.

• Health equity play with immediate deployment pathway: The technology requires only standard smartphone microphones and novice-user operation, positioning it for rapid adoption across 100+ million COPD patients in China alone and similar underserved populations globally where infrastructure and specialist availability are constraints.

3. Predictive modeling & mechanistic validation of synergistic pimodivir combinations for anti-influenza therapy via PB2cap affinity boost

• Machine learning-driven synergy screening significantly reduces development burden: The study’s computational framework screened 8 established antivirals against 1,612 investigational compounds to identify pimodivir + epinephrine/L-adrenaline combinations, demonstrating how ML models can replace labor-intensive experimental validation and accelerate rational combination therapy design for resistant strains.

• Addresses critical resistance gaps in current antiviral arsenal: With >99% of H3N2 and H1N1 strains showing amantadine resistance and oseltamivir-resistant strains already detected (2.14% in China), this synergistic combination approach offers a concrete pathway to overcome cross-resistance—a key unmet clinical need for pandemic preparedness.

• Mechanistic validation through PB2cap binding affinity provides clinical credibility: The study goes beyond prediction by confirming increased binding affinity and viral suppression experimentally, with multiple synergy scoring methods validating results—establishing a reproducible template for developing and validating combination antivirals against RNA viruses beyond influenza.

4. Whole-Genome Sequencing to Identify Bacterial Transmission in Neonates

• Staffing directly impacts infection control outcomes: Full-time nurse staffing reduces transmission-linked colonization risk by 72% (OR 0.28), demonstrating that investment in adequate nursing capacity is a concrete, measurable infection prevention strategy for NICUs—actionable for hospital administrators evaluating staffing budgets.

• Whole-genome sequencing enables precision outbreak detection: WGS identified 37 transmission clusters and linked 34% of colonizations to transmission events, enabling targeted interventions rather than broad protocols; this diagnostic capability should inform NICU protocols for suspected nosocomial spread of multidrug-resistant organisms.

• Vascular catheters are a modifiable risk factor: Catheter use significantly increases transmission risk, while prior antibiotic exposure reduces it by 59% (OR 0.41)—suggesting clinical teams should evaluate catheter necessity and timing, and consider antimicrobial stewardship as complementary infection prevention strategies in vulnerable neonatal populations.