Headlines

Industry News

- Lilly slightly lowers self-pay prices for single-dose vials of Zepbound

- Biopharma Sentiment Index Q4 2025

- Curative Health Reaches $1.275B Valuation to Disrupt Employer Health Insurance

- DeepHealth Launches Comprehensive AI Breast Suite for End-to-End Cancer Care

- Eko Health’s SENSORA Secures National CMS Payment

- Vandria plots Series B raise to advance Alzheimer’s drug into Phase 2

Clinical Studies & Translational Reports

- CGM in Older Adults With Diabetes and Alzheimer Disease and Related Dementias

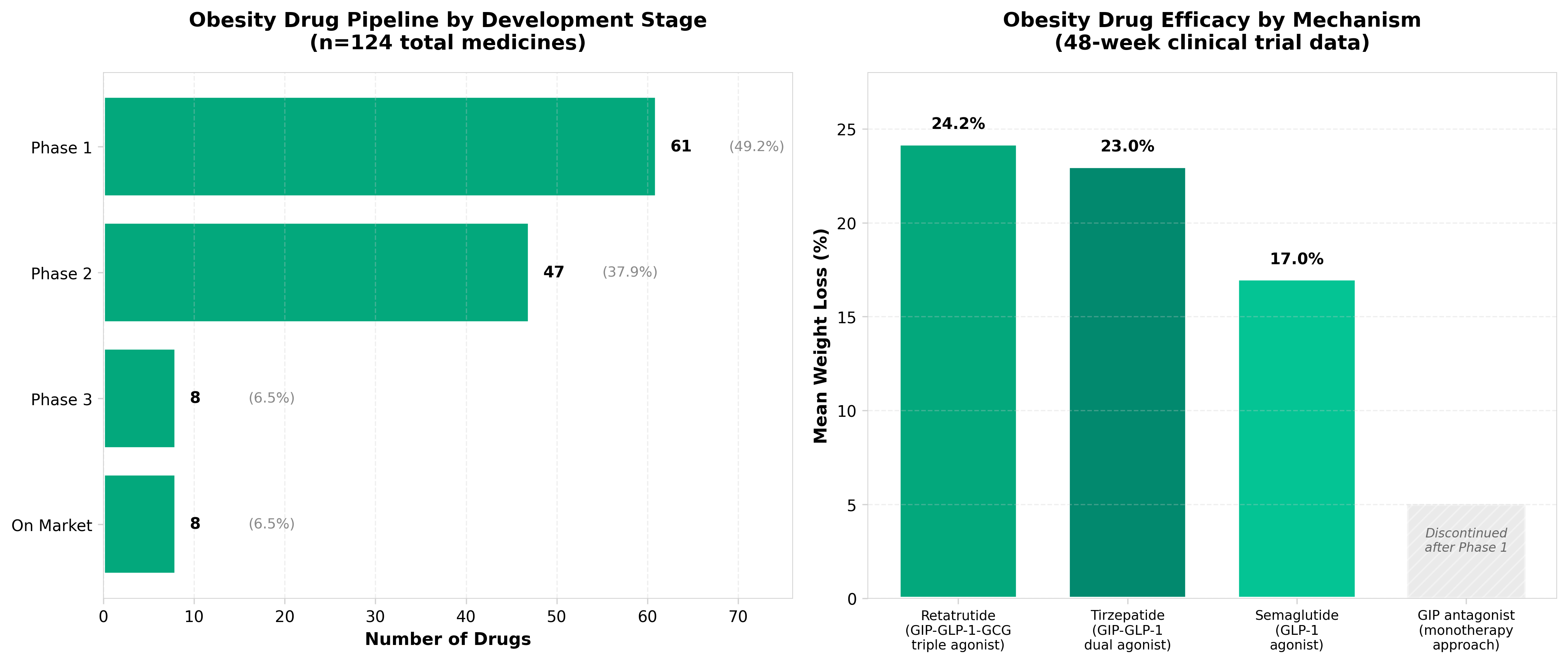

- Helicore stops work on clinical GIP antagonist after Phase 1 results

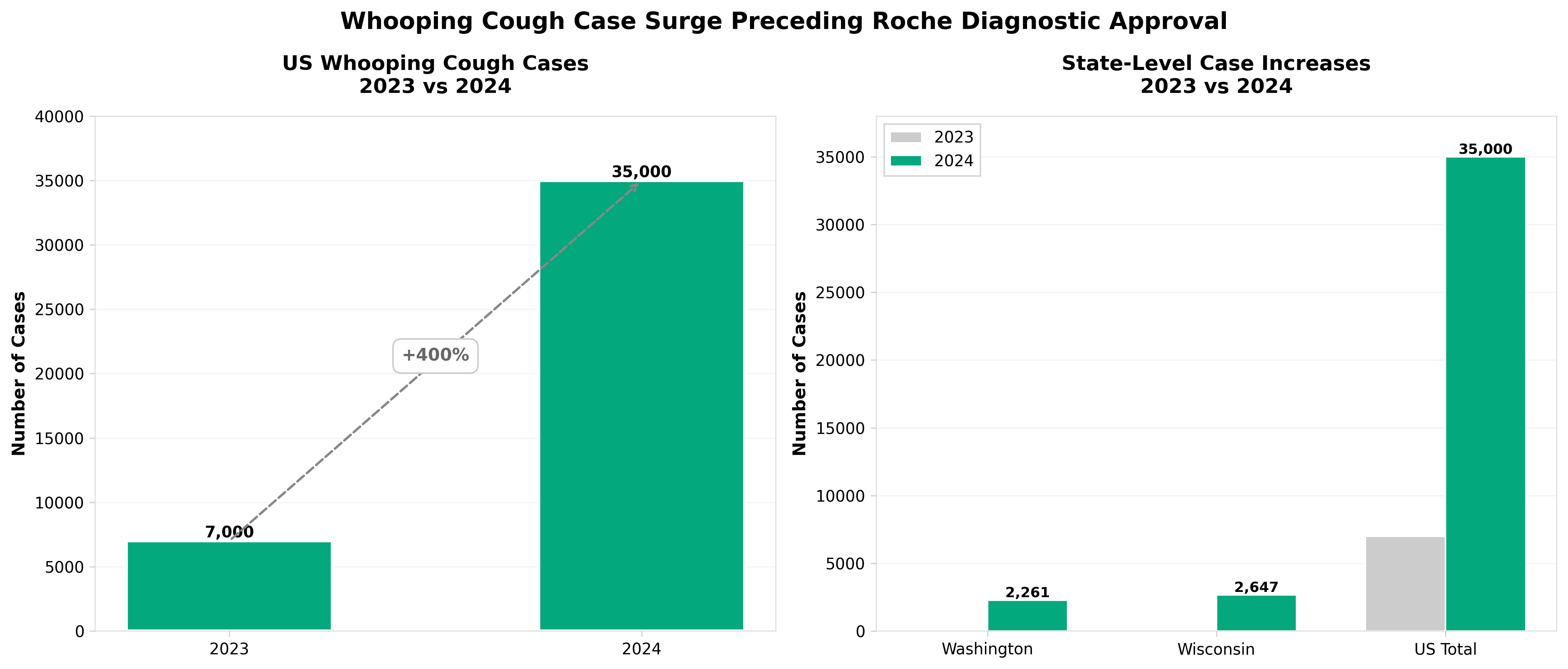

- Roche’s point-of-care whooping cough test greenlighted in US, Europe as cases surge

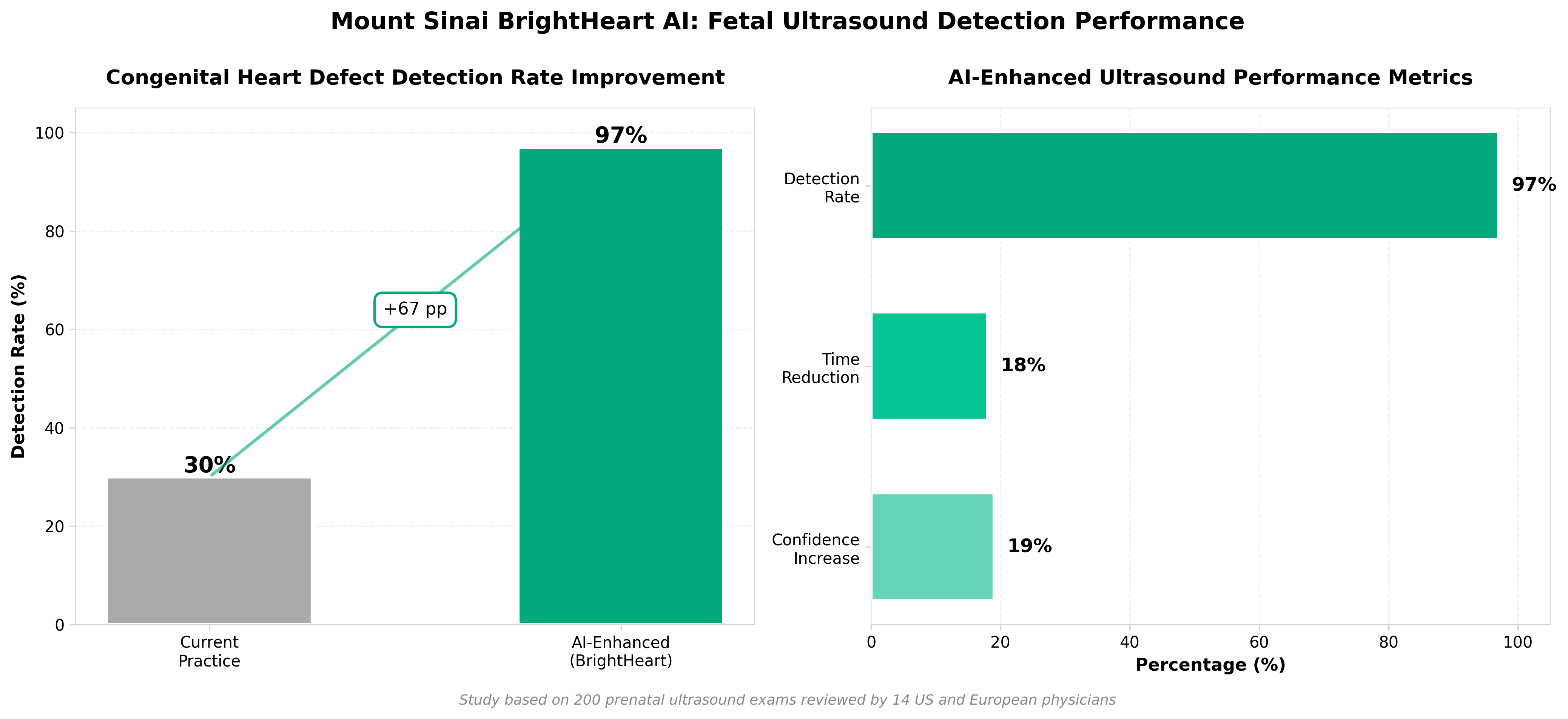

- Mount Sinai Deploys AI-Enhanced Fetal Ultrasounds, Achieves Near-Perfect Detection Rates for Congenital Heart Defects

New Research

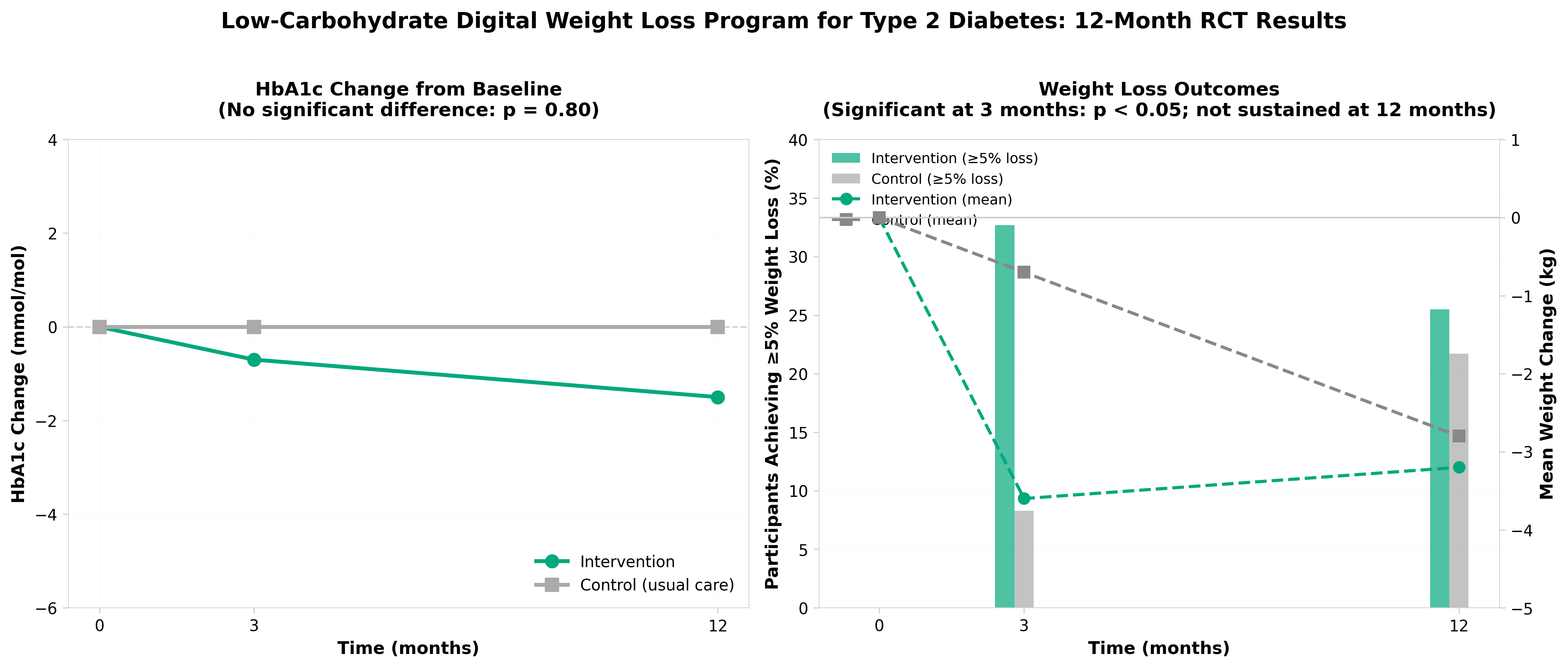

- An RCT of a low-carbohydrate digitally-supported weight loss program

- A randomized study of socially assistive robot effects on patient engagement and care

- Hospital-Level Care at Home for Adults Living in Rural Settings

- Trends in Hospital Resource Use for Children With Complex Chronic Conditions

Industry News

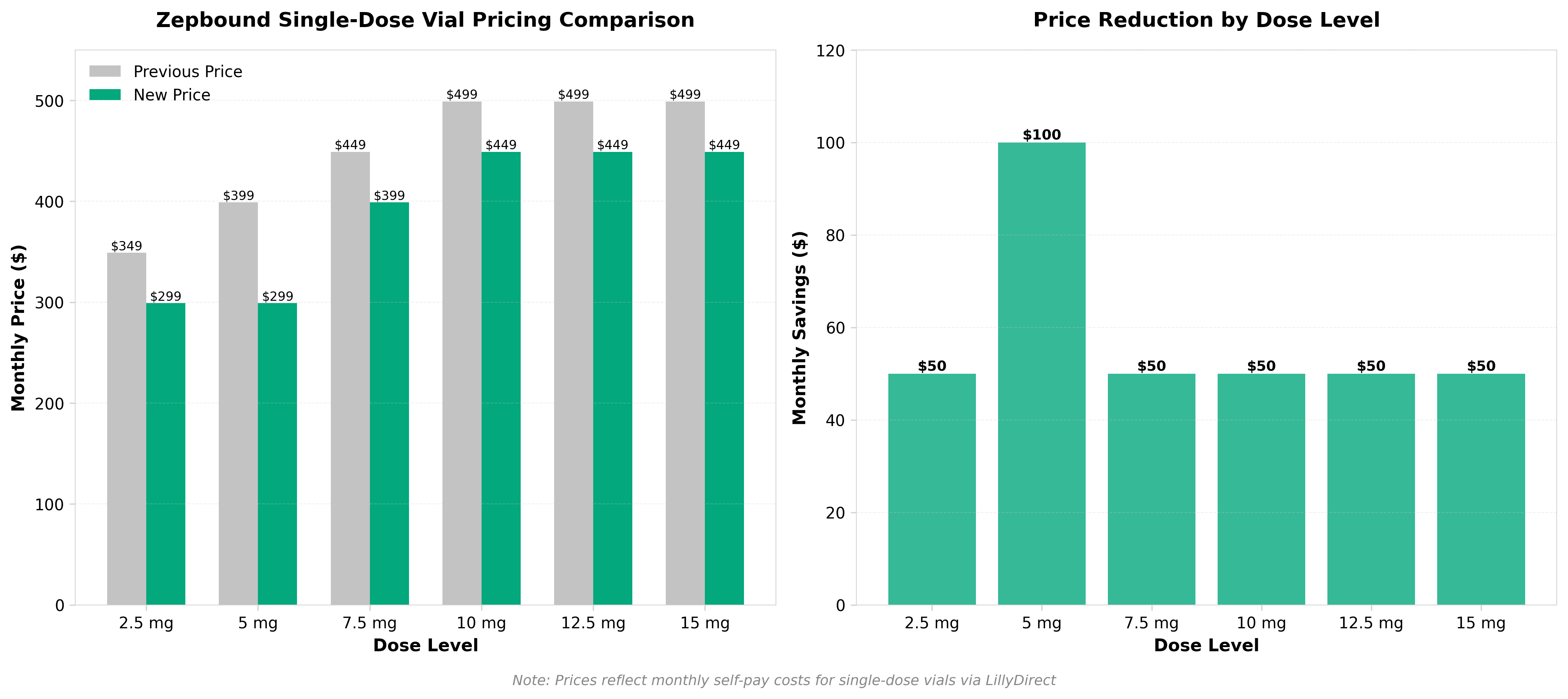

1. Lilly slightly lowers self-pay prices for single-dose vials of Zepbound

• Pricing strategy shift for GLP-1 agonists: Lilly’s $50 reduction on Zepbound single-dose vials (following recent multi-dose pen price cuts) signals competitive pressure to improve self-pay accessibility and likely indicates market saturation concerns as obesity drug adoption accelerates across multiple competitors.

• Self-pay market becoming critical revenue lever: The sequential pricing adjustments within one month demonstrate that out-of-pocket costs are a key adoption barrier; companies are now strategically managing self-pay pricing separately from insurance-covered channels to capture patient volume and market share in the high-growth obesity indication.

• Vial vs. pen distribution strategy implications: Maintaining distinct pricing for single-dose vials versus multi-dose pens suggests Lilly is targeting different patient segments (likely convenience-focused vs. cost-conscious users), requiring companies to optimize manufacturing and supply chain flexibility across formulation types.

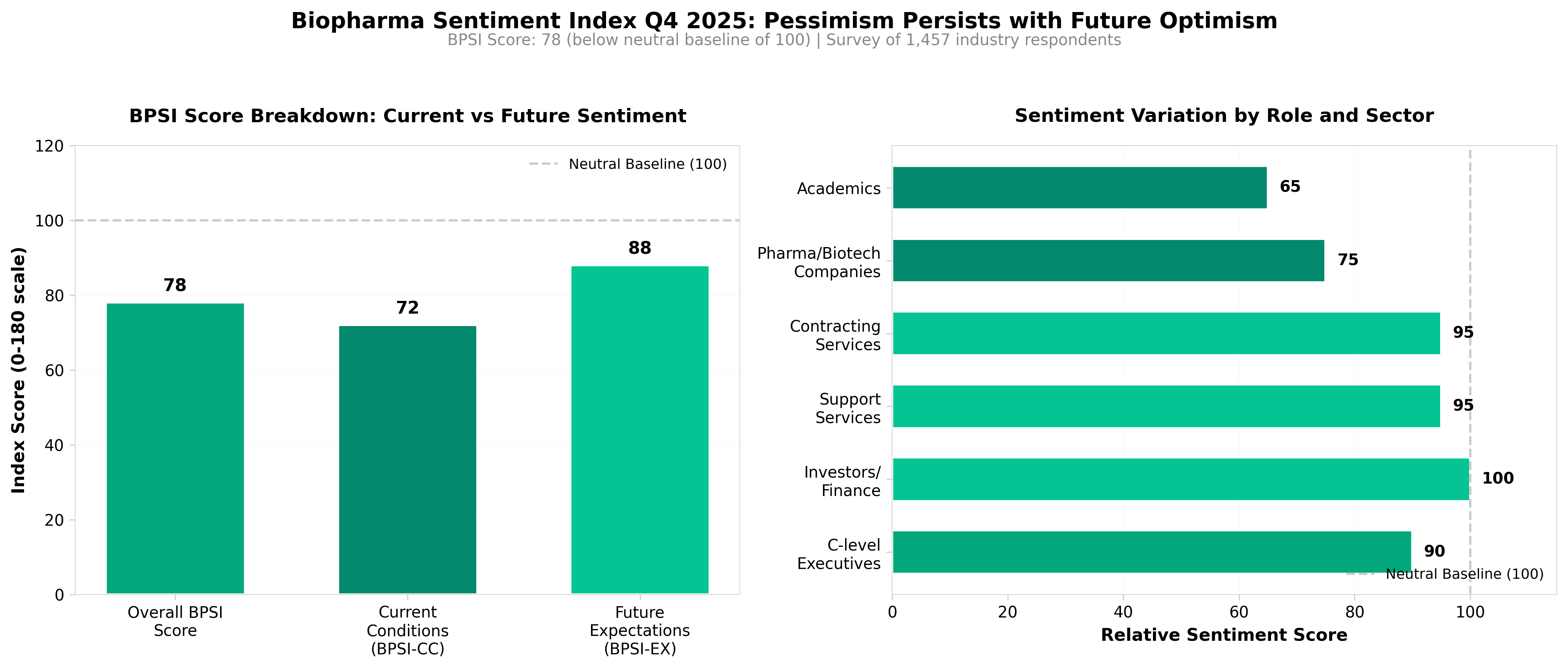

2. Biopharma Sentiment Index | Q4 2025

• Sector-wide pessimism persists despite recovery signals. The inaugural Biopharma Sentiment Index (BPSI) indicates the industry remains in negative sentiment territory, suggesting sustained headwinds in financing, M&A activity, and investor confidence that will likely continue constraining capital availability for mid-stage companies through Q4 2025.

• Sentiment shifts drive material capital allocation changes. Since confidence is identified as a core operational driver alongside science and capital, shifts in the BPSI could serve as a leading indicator for funding cycles—professionals should monitor quarterly index movements to anticipate changes in portfolio prioritization and investment strategy adjustments.

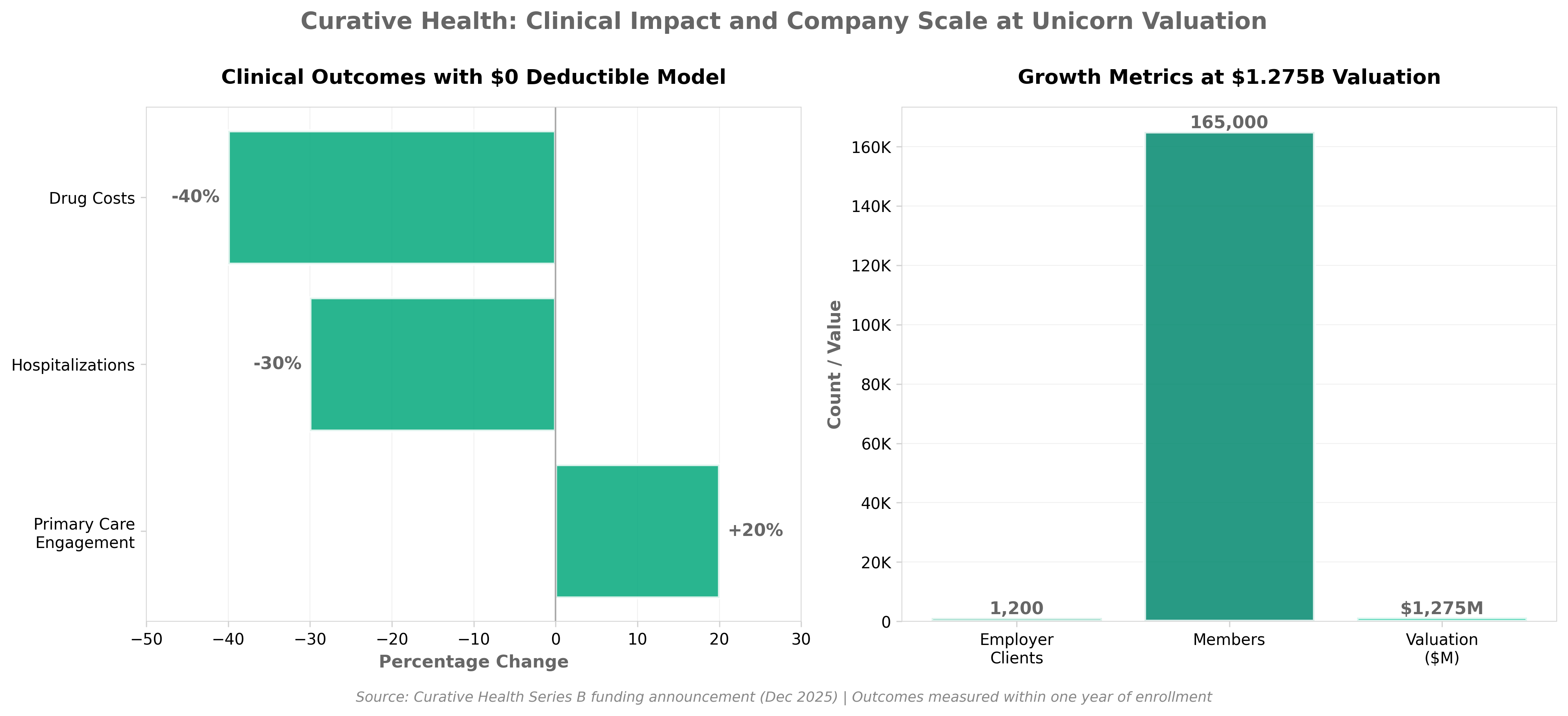

3. Curative Health Raises $150M, Reaches $1.275B Valuation to Disrupt Employer Health Insurance with AI and $0 Deductibles

• AI-Driven Insurance Model Achieving Scale: Curative’s $1.275B unicorn valuation with $150M Series B demonstrates investor confidence in algorithmic-based health plan management as a viable alternative to traditional underwriting, suggesting AI-driven risk assessment and cost optimization are becoming commercially viable at enterprise scale.

• Zero-Deductible Plans Moving into Mainstream: The company’s core offering of $0 out-of-pocket costs signals a potential market shift toward transparent, upfront pricing models in employer health plans; industry professionals should monitor adoption rates and claims data to assess whether this model improves member retention and reduces administrative overhead versus traditional plans.

• Direct Disruption of Employer Insurance Market: With substantial funding and unicorn status, Curative is positioned to compete directly with legacy carriers for self-insured employer contracts; benefits teams should evaluate whether alternative health plan models offer cost or utilization advantages, particularly regarding predictability and member engagement metrics.

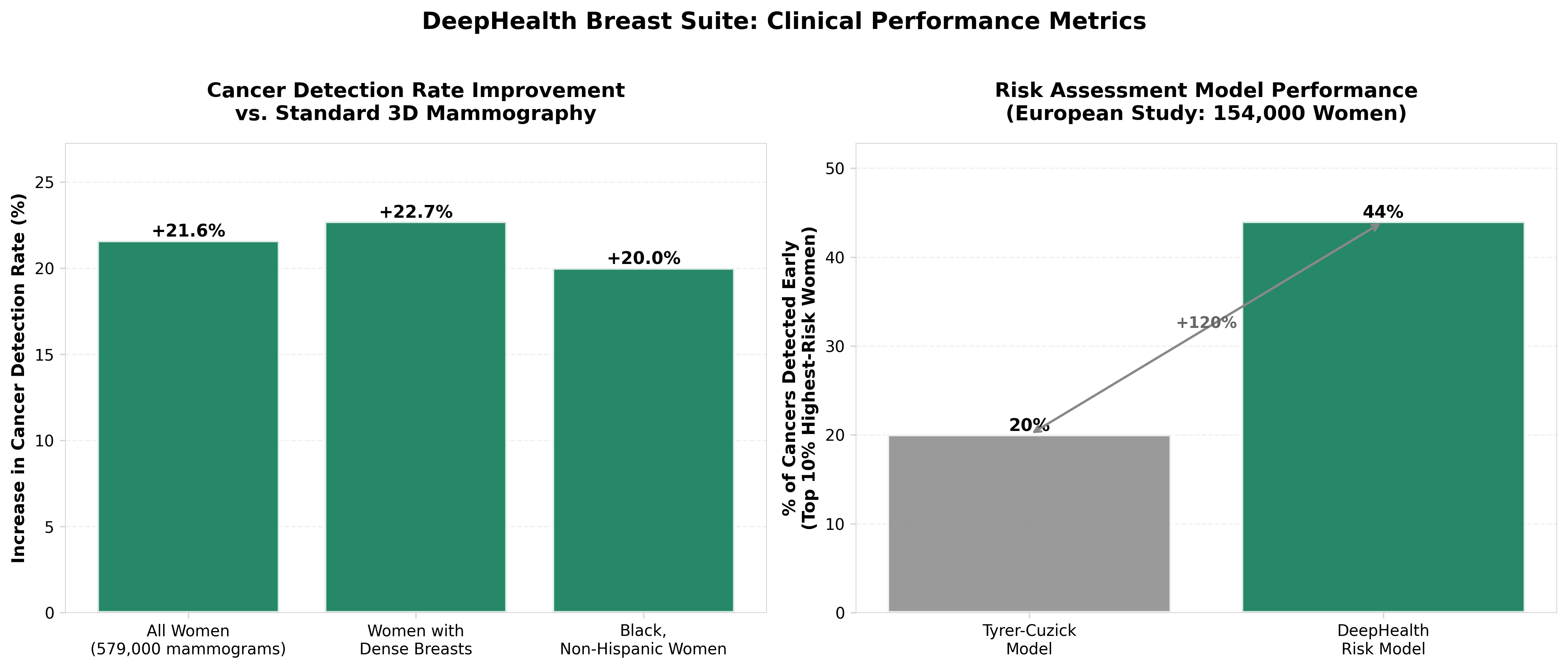

4. DeepHealth Launches Comprehensive AI Breast Suite for End-to-End Cancer Care

• Integrated Platform Strategy: DeepHealth’s modular, end-to-end approach consolidates three critical functions—cancer detection, breast density assessment, and risk stratification—into one system, reducing fragmentation in clinical workflows and potentially improving adoption rates versus single-use point solutions.

• RadNet’s Vertical Integration Play: As a RadNet subsidiary, this launch represents strategic vertical integration of AI capabilities within an established imaging network, positioning the company to capture both software licensing revenue and increased imaging volume through earlier disease detection and improved stage outcomes.

• Cloud-First Architecture Advantage: The cloud-based infrastructure enables scalability across distributed imaging centers and supports real-world evidence generation at scale, critical for ongoing regulatory validation and competitive differentiation in an increasingly crowded AI imaging market.

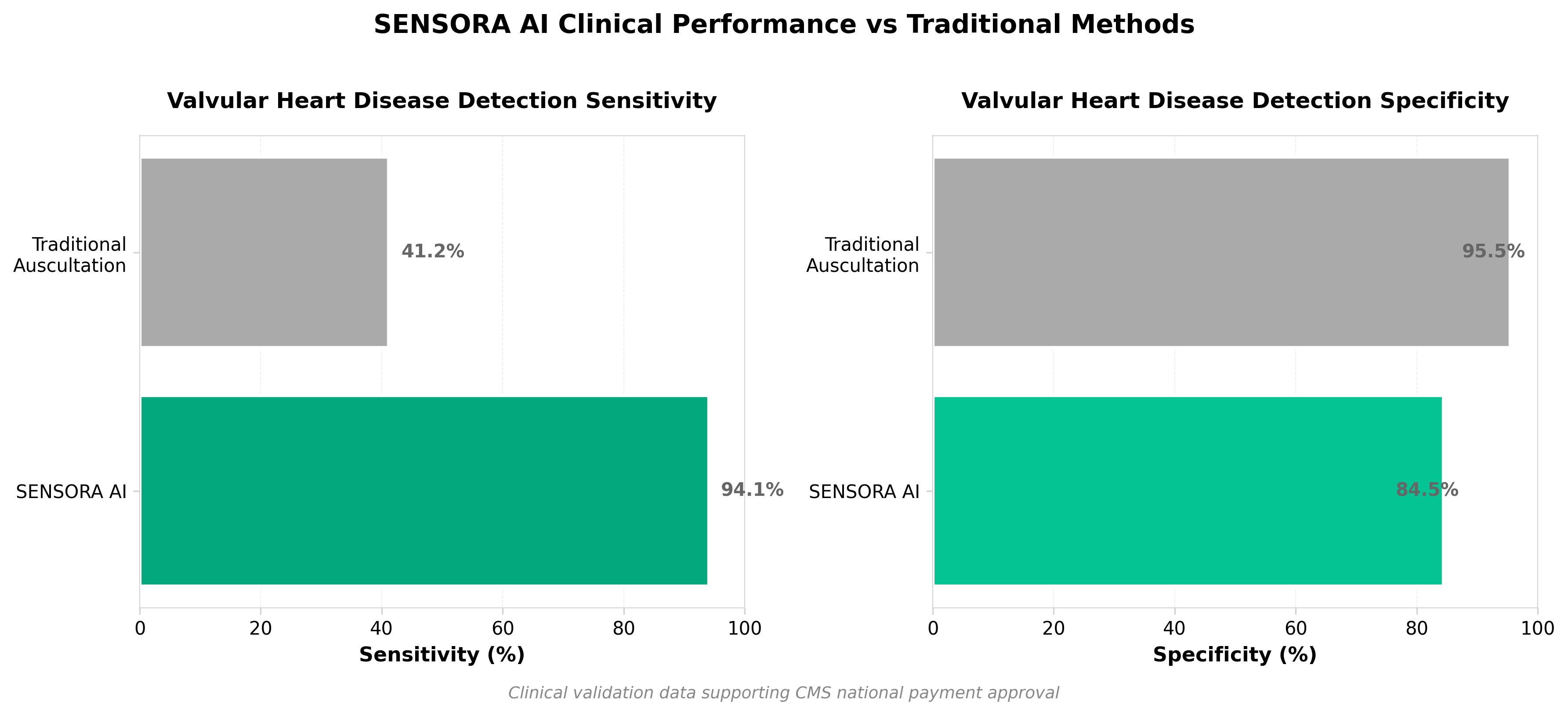

5. Eko Health’s SENSORA Secures National CMS Payment, Paving the Way for Widespread AI Cardiac Screening

• CMS Reimbursement ($128.90/use) removes adoption barrier for hospitals: The OPPS payment finalization under CPT code 0962T creates a financially viable pathway for mainstream deployment across outpatient settings, directly addressing the adoption friction that typically delays AI-medical device penetration in healthcare systems.

• 94.1% sensitivity vs. 41.2% traditional method validates clinical superiority: SENSORA’s doubled detection rate for valvular heart disease over standard auscultation provides quantifiable evidence justifying provider investment and payer reimbursement—critical for defending adoption decisions during budget planning cycles.

• 650,000+ devices already in market position Eko for rapid scaling: With established distribution and 600,000+ active providers, the CMS approval removes the final regulatory/financial constraint, enabling accelerated volume growth and market consolidation before competing AI cardiac screening platforms secure similar reimbursement authorization.

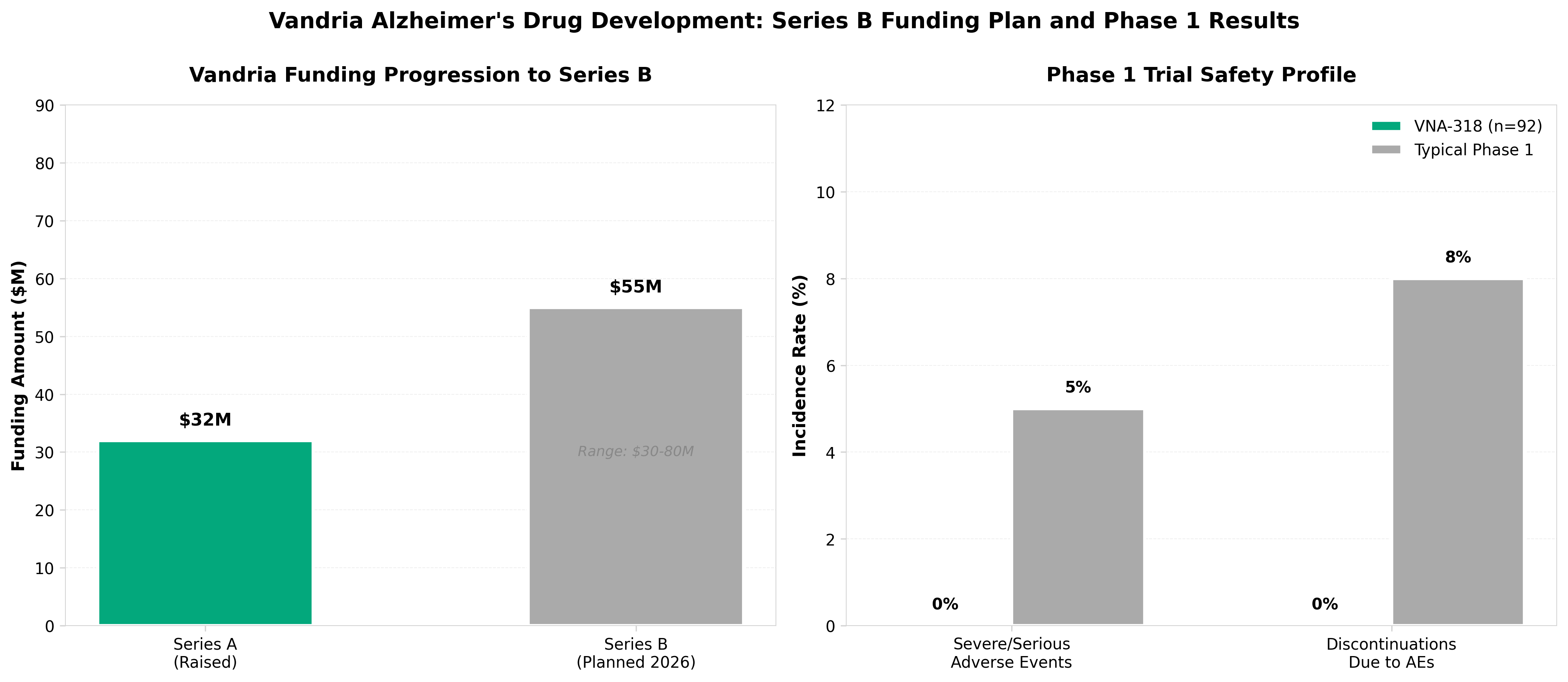

6. Vandria plots Series B raise to advance Alzheimer’s drug into Phase 2

• Exceptional Phase 1 safety profile de-risks Series B: VNA-318 achieved zero serious adverse events and zero discontinuations across 92 subjects with statistically significant biomarker engagement (p<0.001), positioning Vandria competitively against an Alzheimer’s pipeline with a 99.6% historical failure rate and justifying planned Series B raise in 2026.

• $6B→$20.7B market expansion creates 12-year funding window: The Alzheimer’s market is projected to grow at 12% CAGR through 2035 (reaching ~$20.7B), giving Vandria a compressed timeline to advance Phase 2 and achieve proof-of-concept before competitive launches saturate the space with 48 Phase 3 trials already underway.

• Series B target of $30-80M aligns with industry benchmarks: Vandria’s $32M Series A positions it to raise a standard Series B (typical $30-80M range) to fund Phase 2 proof-of-concept trials, with clear capital efficiency milestones needed to attract investors amid increased biotech funding selectivity.

Clinical Studies & Translational Reports

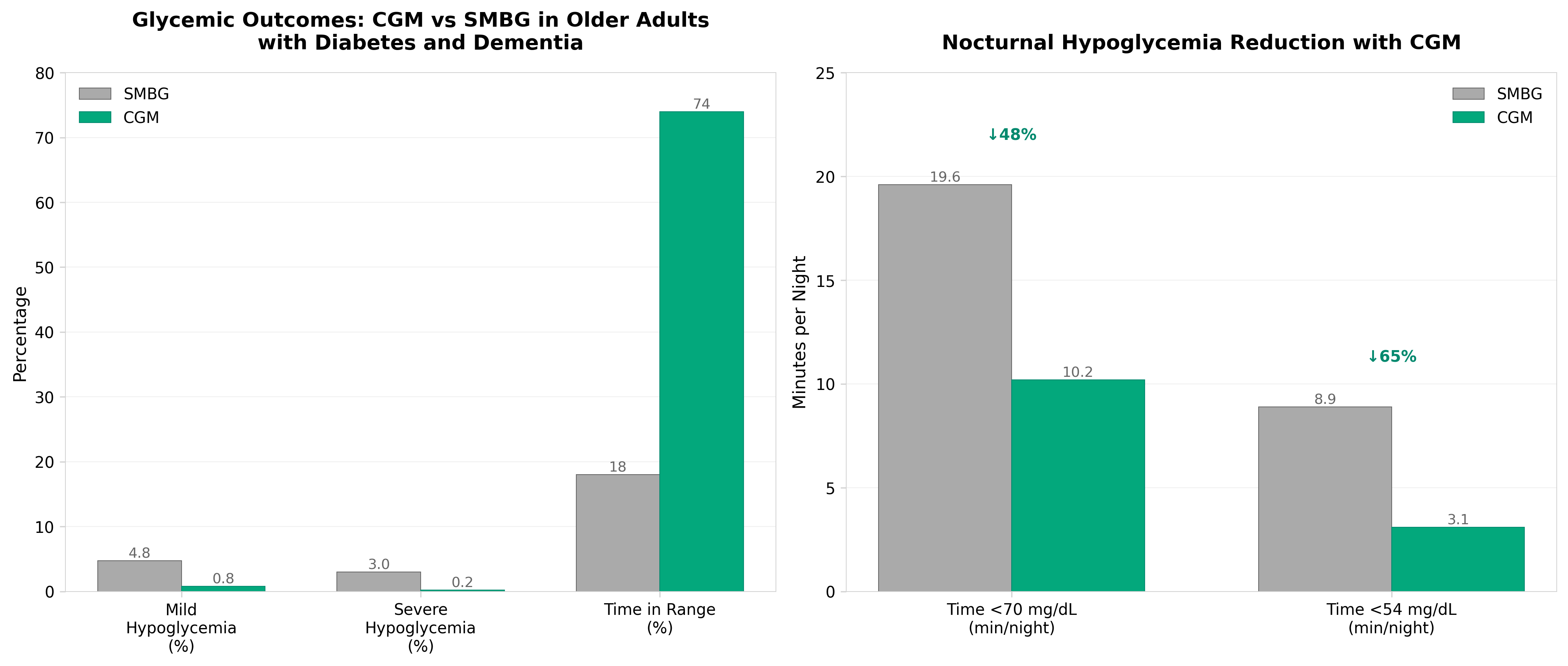

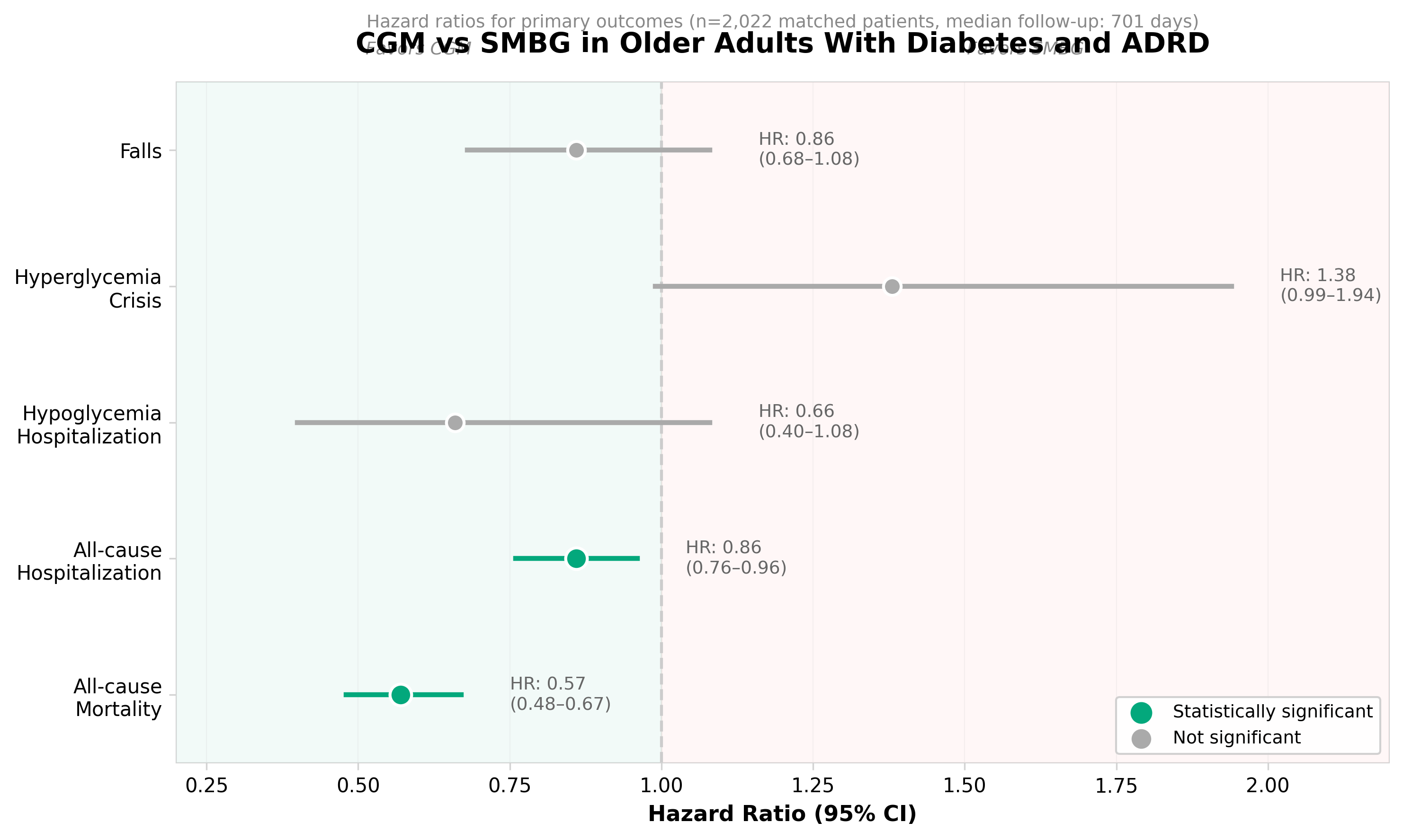

1. CGM in Older Adults With Diabetes and Alzheimer Disease and Related Dementias

• CGM demonstrates potential to reduce severe hypoglycemic events in a high-risk population. Older adults with both diabetes and dementia face compounded medication management challenges; evidence that CGM reduces dangerous blood sugar fluctuations could expand reimbursement justifications and market penetration in long-term care and assisted living facilities.

• Cognitive impairment creates distinct CGM usability barriers requiring product redesign. This population’s inability to self-manage alerts and data interpretation highlights a commercial opportunity for caregiver-centric monitoring systems and integrated care platforms that bypass patient cognition, positioning early movers as solutions for an underserved demographic segment.

• Study addresses a previously under-researched population in CGM literature. Establishing safety and efficacy data in insulin-treated dementia patients fills a regulatory and clinical evidence gap, enabling manufacturers to pursue label expansions and supporting payer discussions around CGM coverage criteria for cognitively impaired populations.

2. Helicore stops work on clinical GIP antagonist after Phase 1 results

• GIP antagonist approach shows limited clinical viability: Helicore’s decision to halt its lead candidate within 12 months post-launch signals that GIP antagonism may not deliver sufficient efficacy or safety signals for obesity treatment, potentially redirecting industry R&D investment away from this mechanism toward alternative pathways (GLP-1, dual agonists, etc.).

• Pipeline diversification becomes critical survival strategy: The pivot to other obesity candidates demonstrates that single-asset dependency in crowded therapeutic areas poses unacceptable risk; biotech companies must maintain multiple mechanistic approaches to obesity to maintain investor confidence and operational viability.

• Phase 1 failure carries significant cost implications: The rapid termination suggests Phase 1 data was sufficiently negative to warrant immediate program discontinuation rather than advancement, highlighting the importance of rigorous early-stage biomarker and PK/PD validation before scaling clinical investments in competitive indications.

3. Roche’s point-of-care whooping cough test greenlighted in US, Europe as cases surge

• Roche’s rapid PCR test (<15 minutes) addresses a critical diagnostic gap in point-of-care settings, positioning the company to capture market share as whooping cough resurgence drives demand for faster turnaround diagnostics in decentralized care environments.

• Dual regulatory clearance (US and Europe) signals strong commercial potential and indicates rising clinical need for pertussis diagnostics—professionals should monitor adoption rates in primary care to assess broader market expansion for rapid infectious disease PCR platforms.

• The shift toward decentralized diagnostics in emergency departments and clinics reflects industry movement away from centralized lab testing; companies developing point-of-care PCR capabilities for other respiratory pathogens may see accelerated validation timelines and reimbursement pathways.

4. Mount Sinai Deploys AI-Enhanced Fetal Ultrasounds, Achieves Near-Perfect Detection Rates for Congenital Heart Defects

• Clinical Performance Creates Immediate Adoption Pathway: AI-assisted detection reached 97% for major congenital heart defects while reducing reading time by 18% and increasing clinician confidence by 19%—metrics that directly improve departmental workflows and justify rapid implementation across health systems without requiring extensive validation studies.

• Addresses Critical Detection Gap in Distributed Care Settings: Currently 70% of CHD cases go undetected prenatally; the validated AI technology enables resource-constrained centers and those without fetal heart specialists to achieve near-expert-level diagnostic accuracy, creating a scalable solution to reduce geographic inequity in prenatal diagnosis.

• Multi-Center International Validation Supports Market Expansion: Secondary analysis across 11 global centers on 877 exams demonstrated 98.7% sensitivity and 97.7% specificity, establishing the clinical credibility needed for regulatory approval in additional markets and positioning BrightHeart for rapid international deployment and reimbursement negotiation.

New Research

1. A randomised controlled trial of a low-carbohydrate digitally-supported weight loss programme for type 2 diabetes

• Digital behavioral interventions for T2D show limited sustained efficacy beyond standard care: Despite initial 2.6 kg weight loss at 3 months in the intervention group, benefits were not sustained at 12 months (–0.4 kg), and HbA1c showed no meaningful difference between groups at either timepoint. This challenges the clinical value proposition for NHS-funded digital diabetes programs and suggests that digital delivery alone cannot overcome adherence barriers to dietary behavior change.

• Low-carbohydrate dietary implementation remains a significant execution problem at scale: Only a small, transient reduction in carbohydrate intake was achieved (10% difference at 3 months, non-significant at 12 months), with most participants not achieving the target 20-30% carbohydrate range. The qualitative data reveals the “low-carb” message was poorly communicated and perceived as secondary to general “healthy eating,” indicating that intervention fidelity degrades substantially when deployed outside controlled research settings.

• Hawthorne effect and COVID-era lifestyle changes confound trial interpretation: Control group participants achieved unexpected weight loss (0.7 kg at 3 months, sustained at 12 months), suggesting trial participation itself motivated behavior change independent of intervention content. This finding underscores the need for pragmatic trial designs to account for secular trends in health consciousness and the limitations of observational program

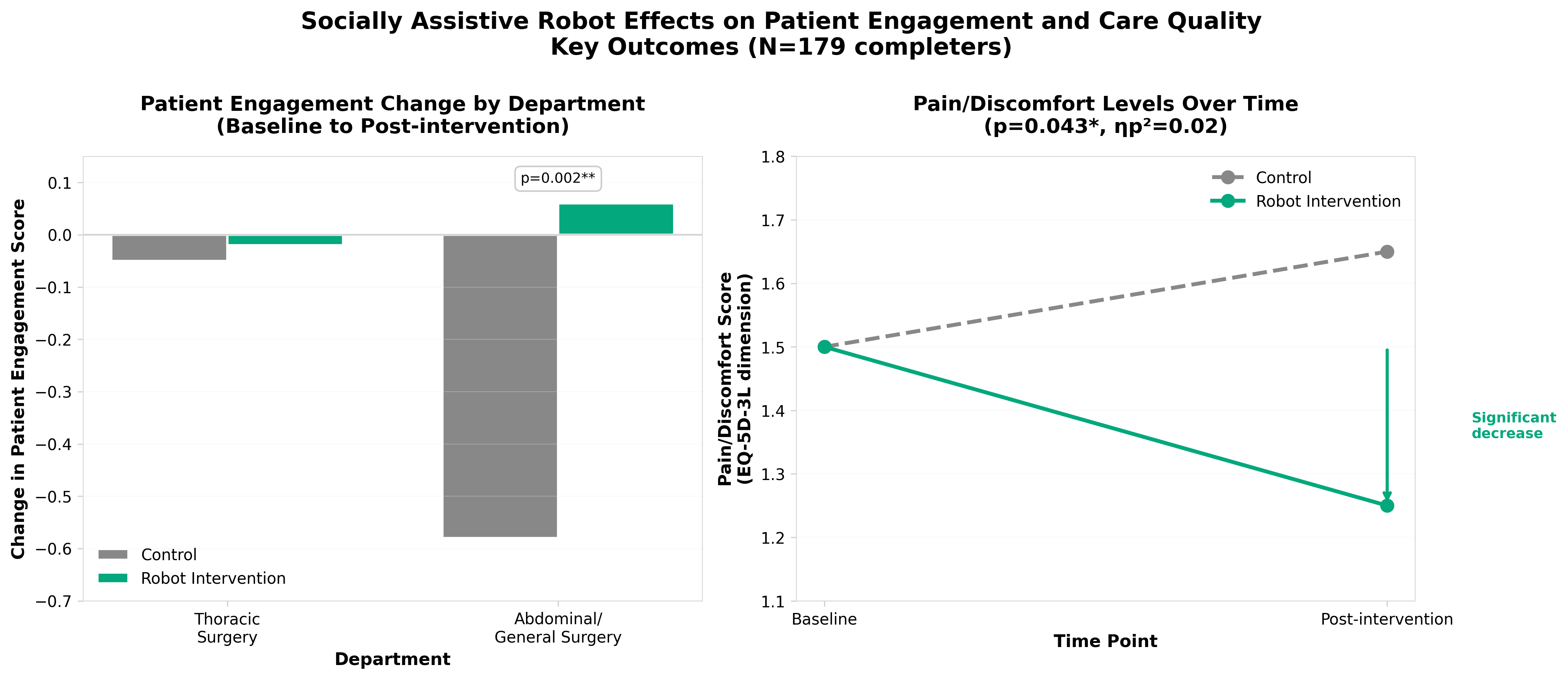

2. A randomized pilot study evaluating socially assistive robot effects on patient engagement and care quality

• Pain management is the only validated clinical benefit: The SAR intervention showed statistically significant improvement in pain/discomfort management (p=0.043), while patient engagement and perceived care quality showed no significant differences between groups, indicating SARs should be deployed for specific, targeted applications rather than broad-spectrum care augmentation.

• Technology acceptance and surgical department type critically determine effectiveness: Patients with high SAR acceptance in abdominal/general surgery showed significantly better engagement outcomes compared to control groups (p=0.022), while thoracic surgery patients showed minimal differences, suggesting implementation strategies must account for procedure-specific recovery trajectories and baseline technology attitudes rather than one-size-fits-all deployment.

• High feasibility demonstrated but early attrition reveals implementation challenges: The study achieved 83-90% retention rates (within typical clinical trial ranges), but 19.5% of intervention patients dropped out before baseline, primarily due to postoperative pain and digital health monitor discomfort, indicating future implementations require streamlined protocols and careful timing of technology introduction during acute recovery periods.

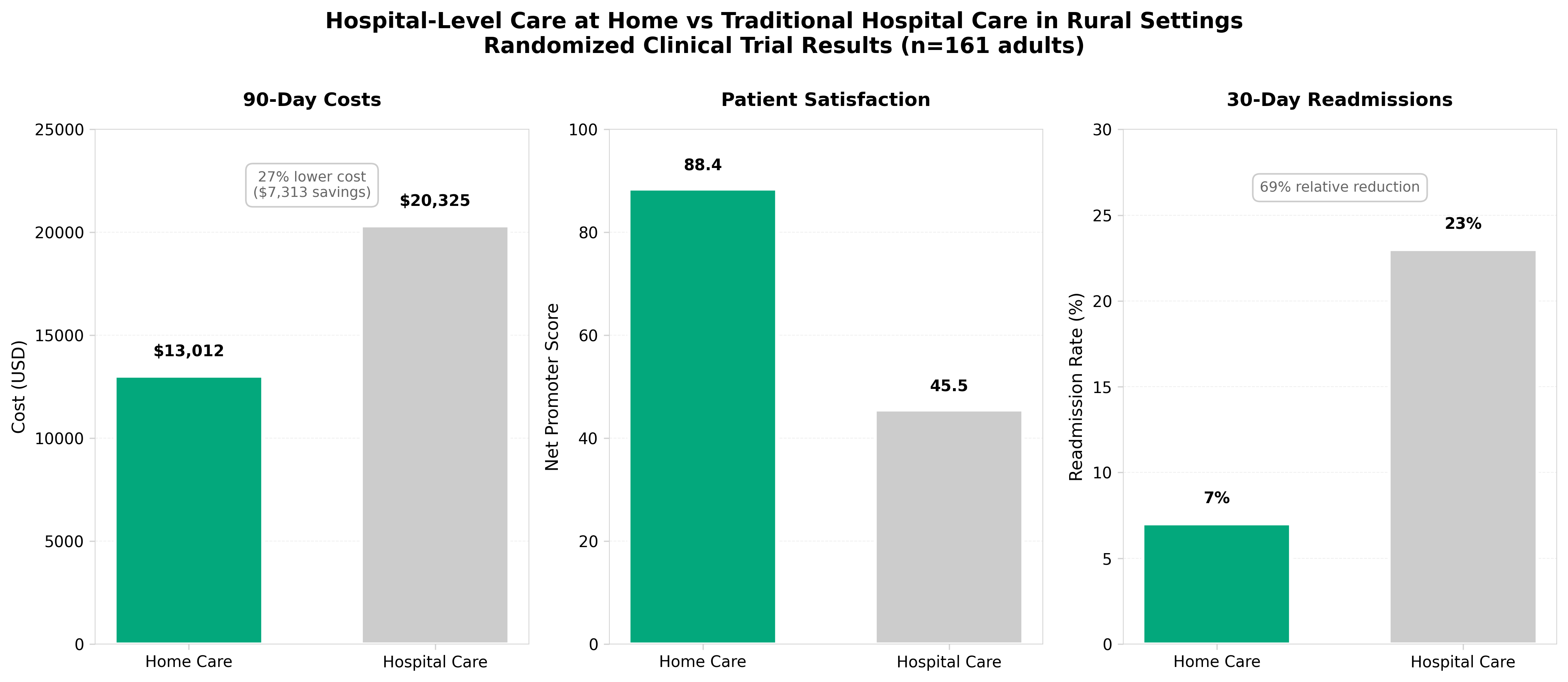

3. Hospital-Level Care at Home for Adults Living in Rural Settings

• Home hospital models demonstrate viability for acute care delivery in underserved rural markets, potentially reducing costly ED visits and hospital admissions while addressing the critical access hospital shortage affecting 60+ million rural Americans.

• Successful implementation requires integrated infrastructure (telehealth capabilities, in-home diagnostics, coordinated logistics) that creates new service line opportunities for health systems and attractive reimbursement models for payers seeking cost-reduction strategies.

• Clinical validation through RCT evidence establishes a foundation for payer coverage expansion and regulatory pathway clarity, positioning early-adopter health systems to capture market share before competitors scale similar programs.

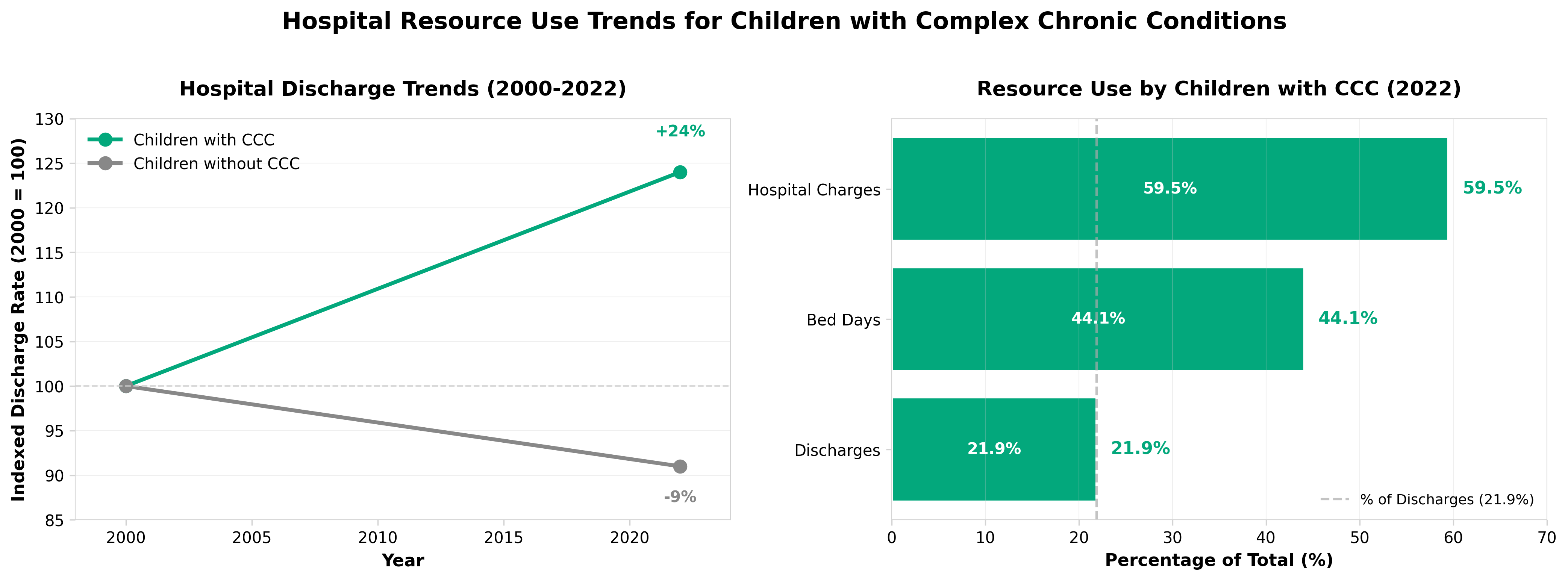

4. Trends in Hospital Resource Use for Children With Complex Chronic Conditions

• Hospital resource utilization for children with complex chronic conditions has shifted significantly from 2000-2022, suggesting evolving care delivery models and payer strategies that warrant review of current pediatric hospital infrastructure and staffing allocations.

• Tracking discharge trends over this 22-year period provides quantifiable benchmarks for pediatric health systems to assess their case mix, length-of-stay patterns, and readmission rates against national trends to identify operational inefficiencies or gaps in outpatient care coordination.

• Understanding resource use patterns in this population is critical for biotech companies developing pediatric therapeutics or digital health solutions, as it reveals where clinical intervention points exist and which hospital departments/services represent the largest cost drivers for payers.